Covid-19 could mean that European companies lose revenues equivalent to 13-24% of EU GDP. We estimate that corporate investment could fall by between 31% and 52%, even in a more favourable scenario. To support economic recovery after coronavirus, our focus should shift from firms’ short-term liquidity needs to a policy response that combines access to credit with long-term equity-type finance to mitigate the trap of too much debt.

By Debora Revoltella, Laurent Maurin and Rozalia Pal

From liquidity shortfalls to reduced net revenues

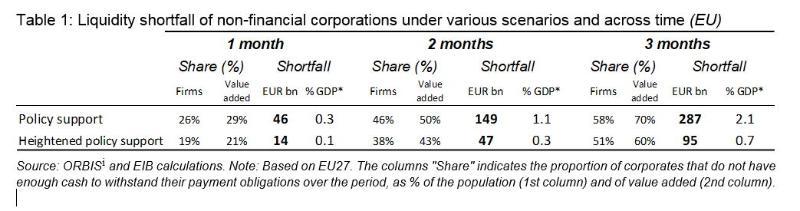

Covid-19 and the related lockdown have taken their toll on the EU corporate sector. A sudden drop in revenues and only partly adjustable costs has led to fast depletion of firms’ cash buffers, even in the context of strong policy intervention. In a previous exercise (EIB 2020a), using an accounting approach, we estimate that even after strong policy intervention, 51-58% of EU firms face liquidity shortfalls after 3 months of lockdown.

The analysis can be compared to other studies that show a large share of firms facing liquidity shortfalls during 2020 (Banerjee et. al 2020, OECD 2020, Demmou et al. 2020 and EC 2020)1. Moreover, policy intervention that reduces firms’ costs during the lockdown has a key role to play to avoid massive bankruptcies. The share of firms with liquidity issue is lower by around 20 percentage points after the implementation of the policy measures (in line with OECD 2020, Demmou et al. 2020).

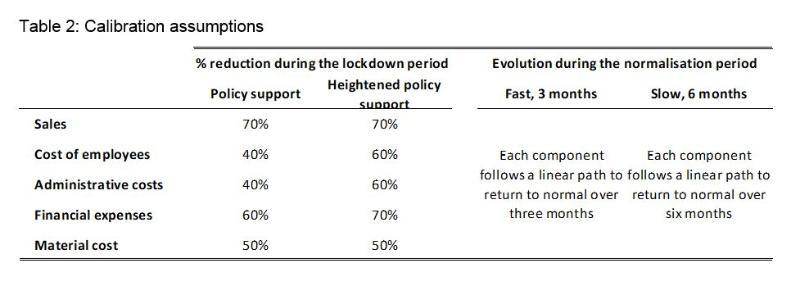

With expectation of a U-shaped recovery, we extend this exercise to assess the possible medium-term strategic choices for firms. We use a comprehensive dataset of more than 1.3 million nonfinancial corporates located in the EU, accounting for around €3 trillion of assets in the final sample. We present four alternative scenarios, to account for (1) strength of the immediate policy support and (2) length of the normalisation period2. The impact of the crisis is illustrated by adjusting each component of net revenues symmetrically for all firms. Under each scenario, we account for the change in corporate activity using the calibrations presented in Table 2.

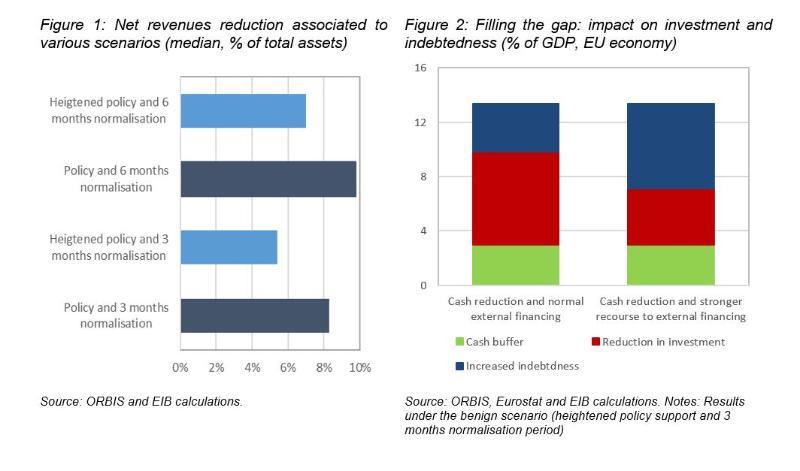

We compute the cumulative net revenue loss for each individual firm. The median reduction in net revenues could range between 5% and 10% of total assets across the four scenarios (Figure 1). SMEs will suffer a reduction between 6% and 11% of assets. Larger corporates would be significantly less impacted, from 2% to 4% of assets. Weighting the estimates by size reduces the overall decline in net revenues to 4% to 8% of total assets, a loss between €1.9 trillion and €3.4 trillion, or from 13% to 24% of EU GDP.

A trade-off between investment and leverage

We focus on the most benign scenario (heightened policy support and 3 months normalisation) and consider a simplified accounting identity to illustrate the impact of lower revenues on the main balance sheet components3.The simplified identity assumes that all earnings are retained. Net revenues finance the accumulation of cash and liquid assets, real investment, and debt reduction. Hence, in this framework, lower net revenues can result in reduced cash balance, increased indebtedness and lower investment.

Cash buffers can absorb a small part of the reduction in net revenues, especially as EU corporates entered the crisis with sizeable cash positions. During the lockdown period, these positions have decreased, but after the crisis it is unlikely that most firms will fully restore their cash positions. We estimate that during the Lehman and sovereign debt crises, cash positions were reduced by 2% of GDP. According to current forecasts, during the Covid-19 crisis, output will be reduced by up to twice as much as during the financial crises. Moreover, given the current very low interest rate environment, the return on cash and liquid assets is almost nil. Hence, we assume that following the Covid-19 crisis, cash positions will absorb 3% of GDP of the loss in net revenues.

EU corporate investment shrinks by 31 to 52% while corporate indebtedness rises by 4% to 6% of GDP (Figure 2). According to the EIB Investment Survey, two thirds of EU corporate investment is financed internally. Hence, after drawing on cash positions, around two thirds of the losses in net revenues (which, after drawing on cash positions represent 10% of GDP) would be absorbed by lower investment, a reduction of 7% of GDP, equivalent to a decline of 52% in corporate investment. Debt would also contribute to fill up the gap, rising by around 4% of GDP. Alternatively, corporations could increase their access to external finance. Assuming that the whole sample of firms tap external finance (even those that do not do so in normal times), the share of external financing would rise from one third to 60% of total financing4. Investment would then be reduced by 4% of GDP (a fall of 31% compared to the level in 2019) but indebtedness would increase by 6% of GDP. The fall in corporate investment would be around twice that recorded during the financial crisis, when corporate investment fell by 19%. This is in line with forecasts that project a much higher impact on GDP, and with the EC findings of a cumulative drop in private investment of €831 billion in 2020 and 2021 taken together (see EC 2020).

An optimal sequencing of policy support

Policymakers have acted swiftly, pledging support and stepping up measures to support corporates as developments have unfolded. Wage subsidies, tax deferrals and loan payment moratoria have been alleviating the cash flow problems of firms. All Member States have implemented some form of tax forbearance or some form of wage subsidy. However, these programmes are limited in time, scope and scale, and they do not necessarily specifically target those firms that are most in need.

Central banks, supervisory authorities and governments have deployed specific measures to maintain the credit channel. Announcements on TLTRO and easing on collateral requirements have secured banks’ access to long-term credit through the crisis. Supervision authorities have provided early indications to banks to use capital and liquidity buffers through the crisis, as well as guidance on provisioning through the cycle. This has been complemented by the widespread use of national credit guarantee schemes, and at the EU-level, the set-up of exceptional financing facilities, such as the Pan-European Guarantee Fund.

While preserving access to credit is key in the short term, absorbing more debt poses problems for a sizeable part of the corporate sector in the medium term, due to leverage constraints. A considerable number of European firms are likely to reach excessive levels of financial leverage as the COVID-19 crisis unfolds. As a consequence, a large share of EU firms could start the recovery period with deleveraging pressures. This in turn would have negative consequences on these companies’ ability to carry out investment plans.

Publicly funded equity-type instruments complement loans and guarantees to alleviate the excess leverage problem. The increase in corporate leverage due to the COVID-19 crisis can be limited by the use of equity-type instruments which absorb any losses but also share in any future profits. However, it is not easy to find effective equity instruments, especially for SMEs whose owners are often reluctant to allow external ownership (for a creative academic proposal see Boot et al. 2020). Equity-type instruments are an integral part of the EU recovery plan. The EIB has long experience as an anchor to both the EU venture capital and venture debt markets. Moreover, equity-type instruments are envisaged in the Next Generation EU package through the new Solvency Support Instrument (SSI)5.

Public support to the corporate sector inevitably raises the question of moral hazard and might include a push towards some long-term policy goals. Measures need to be designed carefully. Support measures that restrict direct benefits for existing creditors, e.g. including limiting dividend payments, can contribute to mitigate moral hazard issues. Temporary measures and built-in sunset clauses can help to avoid permanent distortions. In addition, increasingly targeting support and devising measures with “smart conditionality” – linking support to steps that improve firms’ longer-term resilience, such as the adoption of new business processes or digitalisation – can be a way to preserve activity and also strengthen firms’ perspectives going forward.

Conclusions

COVID-19 and the related lockdown have taken their toll on the EU corporate sector, with an emerging medium-term trade-off between investment and leverage. COVID-19 induced a cumulative net revenues loss for EU companies estimated in the range of 13-24% of EU GDP. To compensate for the net revenues loss, EU corporates will face a difficult trade-off between investment and leverage.

The simulations and the trade-off between leverage and investment suggest some optimal sequencing in terms of policy response. While at the inception of the crisis, deferrals and grace periods play a role in preventing firms’ liquidity shortfalls, those measures are temporary by nature. Measures to support access to credit, including guarantee schemes, follow, but create risk of overleveraging. To properly accompany the recovery, policies to ease access to credit should be matched with enhanced instruments for long-term-equity-type financing. As public support to the private sector always raises the question of moral hazard, transparency and incentive compatibility will be crucial to prevent it. Going beyond the immediate liquidity needs of the corporate sector, long-term, equity-type instruments should be considered to avoid excessive corporate leverage and to preserve financial stability.

- The estimated share of firms with liquidity shortfalls after a given period is sensitive to the assumptions made regarding the capacity of firms to adjust their operating costs to a revenue shock and the assumed impact of the policy measures. Consequently, different share of firms presented by other studies is due to the alternative underlying assumptions.

- For more details, see EIB (2020b).

- ∆Net revenues = ∆Cash – ∆Debt – ∆Inv. Where Inv stands for investment. The estimations do not incorporate additional external financing to re-start business activity at the end of lockdown (see Didier et al. 2020 and Gopinath 2020).

- According to the EIBIS, around one-half of corporates access external resources to finance their investment. When they do so, their funding mix consists of 60% of external finance and 40% internal finance (median values).

- The new Solvency Support Instrument (SSI) proposed as part of the European Commission’s Next Generation EU package would work via an EU guarantee of EUR 26bn provided under the European Fund for Strategic Investments (EFSI). For more details on policy instruments for corporations see EIB 2020b.

References

- Banerjee, R, A Illes, E Kharroubi and J M Serena (2020), “Covid-19 and corporate sector liquidity”, BIS Bulletin No. 10, 28 April.

- Boot, A, E Carletti, H Kotz, J P Krahnen, L Pelizzon, M Subrahmanyam (2020), “Coronavirus and financial stability 3.0: Try equity – risk sharing for companies, large and small”, VoxEU, 3 April 2020.

- Boot, A, E Carletti, H Kotz, J P Krahnen, L Pelizzon, M Subrahmanya (2020), "Corona and Financial Stability 4.0: Implementing a European Pandemic Equity Fund", VoxEU, 25 April 2020.

- Demmou L, G Franco, S Calligaris, D Dlugosch (2020), “Corporate sector vulnerabilities during the COVID-19 outbreak: Assessment and policy responses”, VoxEU.org, 23 May 2020.

- Gopinath G (2020), “Limiting the economic fallout of the coronavirus with large targeted policies”, in “Mitigating the COVID economic crisis: Act fast and do whatever it takes”, edited by R. Baldwin and B.W. di Mauro, VoxEU.org eBook, CEPR Press.

- Didier T, F Huneeus, M Larrain and S Schmukler (2020), “Hibernation: Keeping firms afloat during the COVID-19 crisis”, VoxEU.org, 24 April.

- Didier T, F Huneeus, M Larrain and S Schmukler (2020), “Financing Firms in Hibernation during the COVID-19 Pandemic”, World Bank Group Research & Policy Briefs No. 30, 13 April.

- EC (2020), “Identifying Europe’s recovery needs”, Commission Staff working document, 27 May.

- EIB (2020a), Covid-19 economic update, 15 April.

- EIB (2020b), Covid-19 economic update, 10 June.

- OECD (2020), "Corporate sector vulnerabilities during the Covid-19 outbreak: assessment and policy responses", Tackling Coronavirus Series.