An EU technology transformation is needed to boost the economy through innovative finance, better regulation and a stronger single market

Over the last year, concerns re-emerged about the long-term economic outlook in Europe. Investment has been clearly recovering in Europe, thanks to improved access to finance and to monetary policy that has kept interest rates low, but our latest Investment Survey shows that many companies have concerns about the future regarding regulatory issues, the political climate and a shortage of skills for the digital transformation.

The EIB’s latest Investment Report, titled “Retooling Europe’s Economy,” provides a comprehensive analysis of investment trends in Europe. The report, which found several key reasons to be concerned about the future, opens a window on some of the weaknesses in the EU economy, the costs involved if we don’t take action, and what “retooling” is required.

Structural challenges

As I explained in a story on the VoxEU blog, some things are going well for the economy. The intensity of investment in the EU, relative to gross domestic product, is now close to its long-term average. This part of the recovery has included investment in machinery and equipment, as well as investment in homes and other building structures. Monetary and financial conditions have supported this recovery. The cost of borrowing for businesses is still low, and the share of firms in the EIB Investment Survey (EIBIS) that name access to finance as a major impediment to investment is low, at 17%, and falling.

However, strengthening headwinds are causing some people to worry about slowing growth. The Investment Survey, which contacted12,500 firms across Europe, asked what factors might influence investment activities. The number of firms that feel the general economic climate is supporting investment has declined since 2017, while the number of firms considering political and regulatory conditions as negative for investment has substantially increased. This is an early warning sign, with Brexit, rising social tensions, political polarisation and increasing economic risk contributing to rising uncertainty.

Our survey revealed several ways to help Europe’s economy:

- encourage a dynamic, innovative business environment by improving regulatory conditions

- improve the single market, particularly for services, and create the conditions for a truly European digital market

- increase investment in infrastructure and innovation, and adopt new technologies

- work together across countries to improve skills, competitiveness and social inclusion, and coordinate more action at the EU level.

Can the EU technology transformation keep up with the rest of the world?

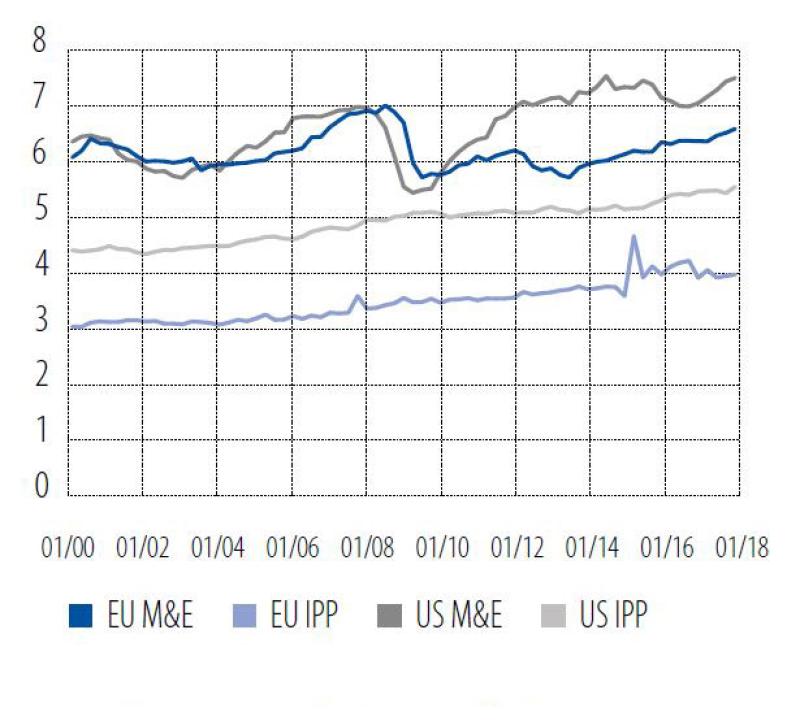

In a period of disruptive technological transformation, Europe’s recovery has been relatively weak, at least in relation to the United States. Since the economic crisis that began around 2008, the gap between EU and US investment in machinery and equipment has widened. While this gap is partially related to the shale gas boom in the US, it raises questions about whether the EU can keep up in terms of technological transformation, and carry out a widespread adoption of new technologies.

Investment gap, EU vs US (machinery & equipment and intangibles % of GDP). Source: Eurostat and OECD statistics.

This gap in tangible investment is even more worrisome when viewed in combination with the well-known gap in investment in intangibles. European firms still fail to invest in different forms of intangibles, such as research and development. Besides R&D, investment in software, skills, and organisational transformation are becoming essential in the new digital world, both in the manufacturing and service sectors.

In innovation, the EU shows a lack of dynamism. Based on the Investment Survey’s data, the EU, compared to the US, has more firms that do not innovate or that only adopt other companies’ innovations. Europe is especially lagging behind in terms of leading innovators, particularly among young firms. This is a symptom of a more static system, where fewer young firms succeed in displacing older rivals.

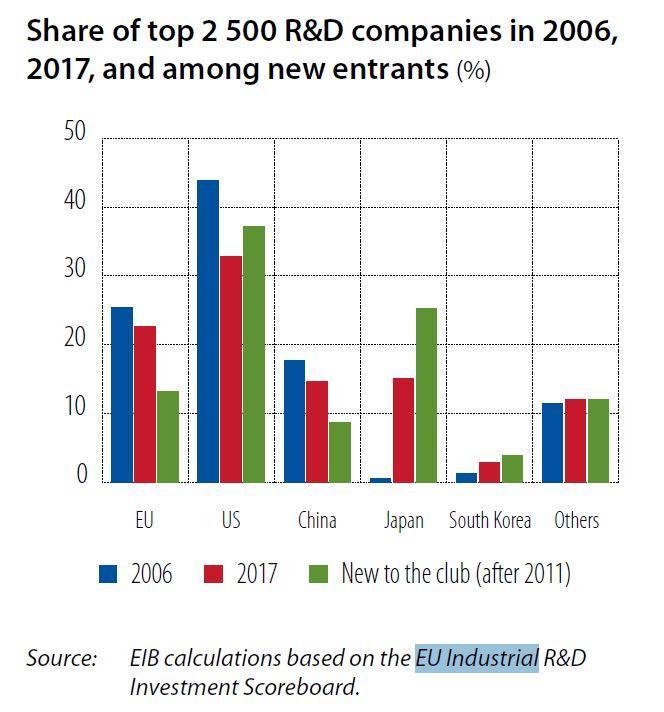

Looking at the top firms globally for R&D expenses, there has been a dramatic rise in China and a lack of dynamism in Europe, with fewer new entrants since 2011 among the top firms. European firms also have a much lower presence in high-tech sectors.

Finance is one of the main constraints for innovation and technological transformation in Europe. The European financial sector is largely based on banks, but banks are not well suited to finance innovation and intangible investments. While the cost of debt is about 400 basis points below its level before the global economic crisis, the cost of equity has not fallen to such an extent. The equity risk premium remains high and the spread between equity and debt is still larger than before the crisis. Private equity, venture capital and listed equity funding all lag behind the US and advanced Asian countries on several fronts, leaving European firms more dependent on bank lending and weakening their resilience to financial shocks.

Financially constrained innovators

Using the Investment Survey’s data to compare innovating firms with non-innovating firms, we found that the innovators have better performance and financial health, yet are significantly more likely to be financially constrained. They are especially dissatisfied with the collateral required for bank loans, as you would expect for firms investing in intangibles such as intellectual property.

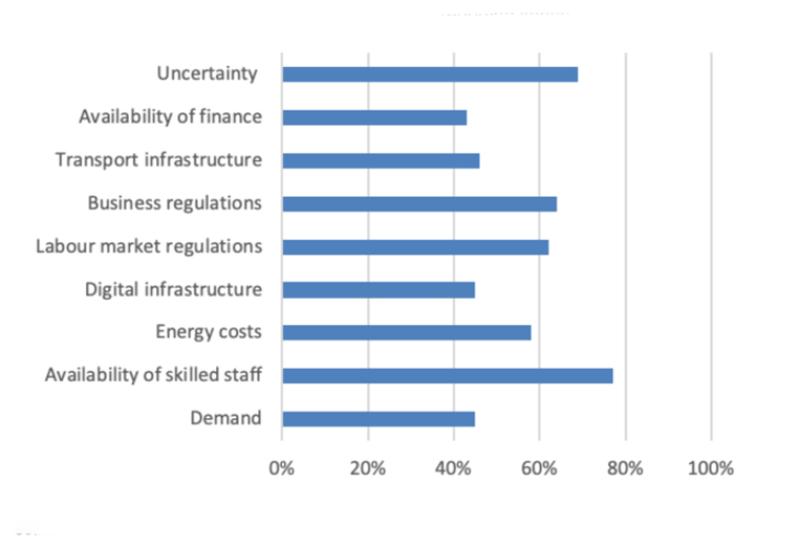

Skills are another constraint: 77% of European firms said that the limited availability of skilled staff impedes investment. This skills gap reflects a structural process of adjustment to changing technology and skills, exacerbated by a tight labour market in many EU countries and migration in Central and Eastern Europe. The firms that are the most innovative are having the hardest time finding skilled staff. Seventy-one percent of EU firms invest in training, but only 21% say that the amount of investment in training has been sufficient. This may partially reflect the difficulty firms face in recognising the benefits of training, so there could be a need for public action in this area.

Long term barriers to investment (% firms reporting impediment to investment) - Source: EIBIS 2018

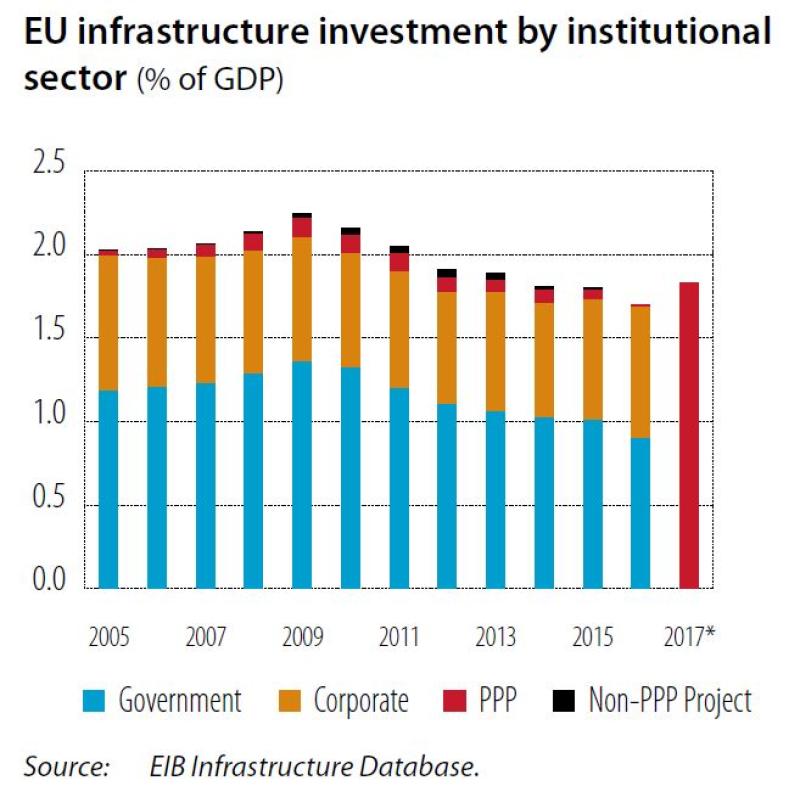

Quality infrastructure is also important for economic growth, but investment in infrastructure in the EU is lagging. At 1.7% of GDP, it is about 25% below its pre-financial crisis level. This does not appear to be because there already is enough infrastructure investment in the EU. One in three large municipalities in Europe say that infrastructure investment is below their needs. Instead, this downturn reflects the public sector’s decision to shift funds away from infrastructure during the crisis. The capabilities to generate infrastructure projects also has been declining. The capacity to plan projects and to generate projects is poor. We need clearer incentives for the private and public sector to cooperate and more support for project planning and preparation.

To fight these weaknesses, the institutional framework will be key. Forty-three percent of municipalities regard technical capacity for planning and project generation as a major obstacle. Difficulties in structuring public-private partnerships mean that incentives for private sector operators are unclear. Firms are three times more likely to innovate and nine times more likely to introduce a patent in regions that have a good institutional framework. Firms also consider business and labour market regulations to be significant impediments to investment.

The cost of inaction is high

Our EIB Investment Survey on digitalisation and skills, covering 1,700 firms in the EU and the US, represents the first direct comparison of digitalisation achievement in the EU and the US. The survey suggests that firms that adopt digital technologies tend to be more productive and innovative, and invest more. They also say that the adoption of digital technologies helps sales: 50% more firms in manufacturing and over 60% more in services say sales would have been lower if they had not adopted digital technologies.

More worryingly, digitalisation appears to be creating a winner-takes-all economic environment. On the one hand, digitalisation is associated with higher prices, suggesting a lack of competition. On the other, the most productive digitalised firms stand out in expecting that digitalisation will lead to a decrease in the competition they face. This suggests that late adoption of digital technologies could have long-lasting effects on competitiveness.

As disruptive technologies become more important, there is a cost of inaction. So far, in the manufacturing sector, European firms have kept pace with their US counterparts in terms of digital adoption, but in the service sector, EU firms are lagging. Moreover, when one looks at the most advanced forms of digitalisation (internet of things, big data, and software development), the gap between Europe and the US is wider.

A response at all levels

Europe’s economy still lacks the ‘tools’ to meet the urgent challenges of the future: remaining globally competitive in the face of rapid innovation and digitalisation, achieving sustainability, and creating an inclusive society. This requires a response at all levels, and not least at the European level. European cooperation is needed to allocate funds where they can be the most productive, overcoming investors’ preference to invest mainly in their home countries. This means improving financial integration through the Capital Markets Union and the Banking Union. It also means making full use of EU institutions and instruments, such as the EIB and the EU budget.

Retooling Europe must be socially and environmentally sustainable, taking into account the impacts of automation on jobs and demand for skills, issues of cybersecurity and data governance, and, not least, the need for a step-change in investment in climate change mitigation.