How technological transformation investment can reinvigorate productivity growth

By Luis de Guindos

On 28 and 29 November, the European Investment Bank and the European Central Bank, in cooperation with the Massachusetts Institute of Technology, Columbia University and SUERF (the European Monetary and Finance Forum) will co-organise a high-level conference on ‘Investment, Technological Transformation and Skills’.

Strong economic growth underpins greater prosperity over the long run. Yet trend growth in the euro area is low, compared with other advanced economies, reflecting an ageing population and recent poor productivity performance. Europe needs to reinvigorate productivity growth to sustain improvements in living standards.

Harnessing the benefits offered by technological advances like digitalisation, robotisation and artificial intelligence is crucial. But firm-level evidence from the Competitiveness Research Network (CompNet) shows that productivity gains remain patchy across all sectors. We need to give firms the right incentives to invest in technology, thereby ensuring that capital and workers migrate from low to high productivity businesses.

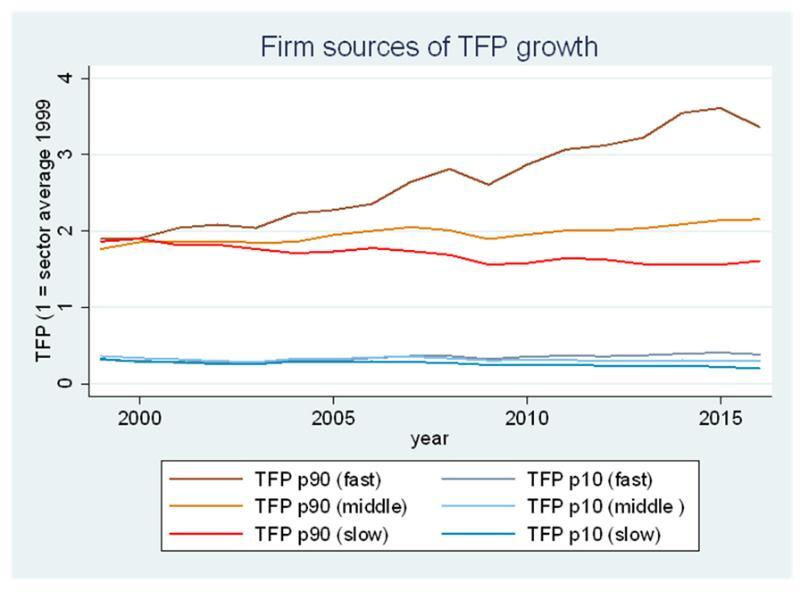

We can illustrate this point by using CompNet data to classify sectors into fast, medium and slow-growing groups based on their total factor productivity growth. We can then explore the dynamics of top-performing firms (90th percentile in terms of productivity) and laggard firms (10th percentile) in each of these three groups over time.

The productivity levels of the top-performing firms in the fastest-growing group are now three times the 1999 sector average (Chart 1). Meanwhile, the productivity of the top firms in the medium group has barely nudged up, while it has actually fallen in the slow-growing group. And the productivity of laggard firms in all three groups has barely changed at all. So the dynamics of firms at the top of the distribution drive the differences between sectors.

Chart 1: Dynamics of high and low productivity firms

Source: Own calculations on the sixth vintage of CompNet data, full sample.

Notes: Total factor productivity (TFP) is indexed to average productivity in 1999, which is the start year. Countries included are: BE, ES, FR, HR, IT, LT, HU, NL, PT, RO, SI, and SE.

Insights derived from the CompNet data suggest a number of promising avenues for boosting productivity growth:

- removing market rigidities to promote competition and encourage firm entry and growth;

- enabling capital, labour and finance to leave low productivity firms;

- ensuring the financial system supports investment in technology.

That cyclical factors such as weak demand and uncertainty weigh on investment is well-known. But structural factors such as weak economic institutions and rigid product and labour markets can also play a negative role. Investment in technology can be encouraged by enhancing the structural and macro conditions favouring labour mobility, market entry and the expansion of productive firms.

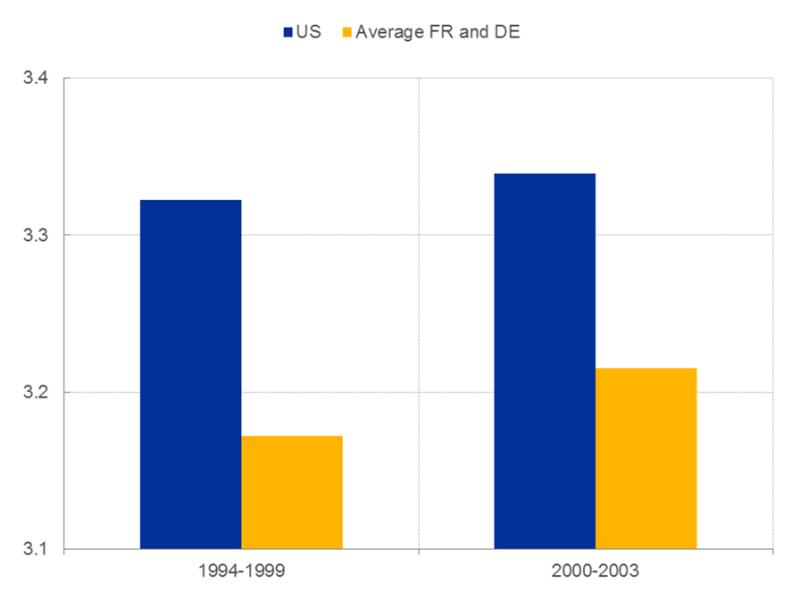

Technology changes how we work. To reap the benefits of technology, managers need to reorganise production processes. Workers need opportunities to reskill in order to move from low to high productivity businesses. Education policies aimed at promoting managerial skills—an area in which the euro area lags behind the United States (Chart 2)—could smooth the transition, and facilities for workers’ life-long learning and retraining are vital.

Chart 2: Managerial skills in the United States and the euro area

Source: Own calculations on Bloom and Van Reenen (2007): “Measuring and explaining management practices across firms and countries”, the Quarterly Journal of Economics, Vol. 122(4).

Note: Survey-based score from 1 (worst) to 5 (best) across 18 key management practices.

To encourage firm entry, Europe needs to create a level playing field in the area of new technology by removing unwarranted protection for incumbents and also settling issues of ownership, tax treatment, property rights and product regulation associated with intellectual assets. But it also needs to reform insolvency regimes to break the adverse impact on productivity from a vicious circle of weak banks and zombie firms.

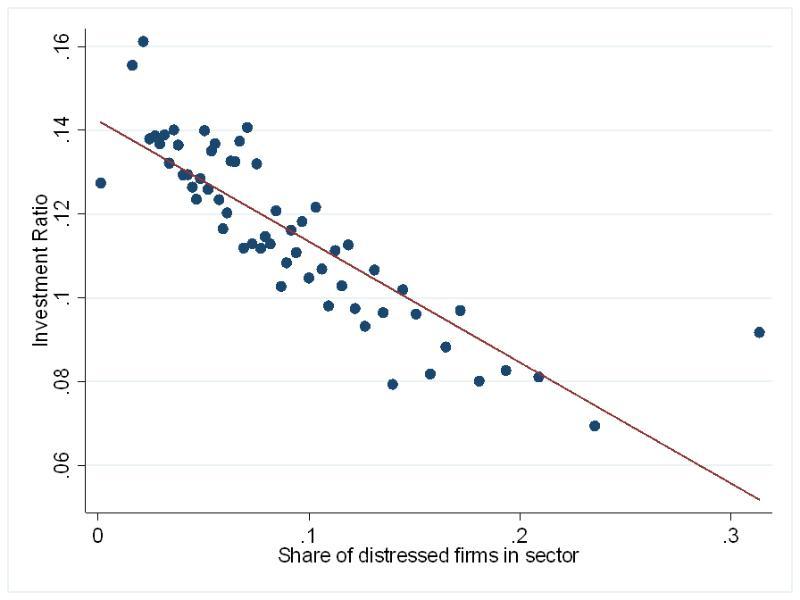

Sectors with a higher proportion of distressed firms (those with interest payments greater than profits for at least three consecutive years) invest less (Chart 3) and also have a higher share of healthy firms that are credit constrained. Bank capital is tied up in lending to low productivity firms, rather than in helping high productivity firms to grow.

Sector investment and share of distressed firms

Source: Sixth vintage of CompNet, full sample.

Notes: The y axis represents the median investment ratio, measured as the growth rate of capital plus depreciation, divided by capital. Distressed firms are firms with interest payments higher than operating profits for three consecutive years, conditional on positive profits. Both variables are measured at the two-digit industry level for a given year and country. Countries included: BE, DK, ES, FR, HR, IT, LT, HU, NL, PT, RO, SI, FI and SE.

The widespread diffusion of technology requires financing that is conducive to innovation and growth. Equity funding in particular is important for growth in high-tech and patent-intensive industries. Investment in new technology and intangibles seems to rely more on firms’ internal funding, given that intangible investment is difficult to use as collateral for external funding.

The timely completion of the capital markets union is therefore of paramount importance. More ambitious policies aimed at increasing the supply of private equity, and especially of early-stage venture capital, are needed. The development of fintech, or new digitally enabled financial products and services, has the potential to expand access to credit and other financial services, in particular for small businesses.

Boosting productivity growth is a fundamental precondition for increasing living standards in Europe over the long term. We need to ensure the widespread diffusion of technology by supporting the flow of capital, workers and finance to where they can be most productively used.

About the author

Luis de Guindos is Vice President of the European Central Bank.