Firms in Europe largely rely on cash reserves and reinvested profits for their financing, while debt is their main source of external finance. They rarely consider external equity. Why?

by Debora Revoltella, European Investment Bank’s chief economist

We ran an experiment to better understand why only 1% of European firms want external equity to play a bigger role in their financing mix. These startling results point to the need for Europe to seriously rethink incentives for firms, with the goal of strengthening economic resilience and fostering innovation.

Europe is in denial. Firms finance investment predominantly through internal sources. External finance represents less than 40% of firms’ investment finance, with bank debt and leasing prevailing. Companies think they can invest and grow without diluting their ownership through external equity financing. The result: lots of firms are reliant on internal finance and bank debt, and they show a sluggish rate of growth.

The full experiment can be followed in a working paper we just published. We gave two different financing choices to a sample of 973 European companies, all of which were planning investments. The offers had varying sizes, interest rates, maturities, collateral requirements, and subordination/equity conditions.

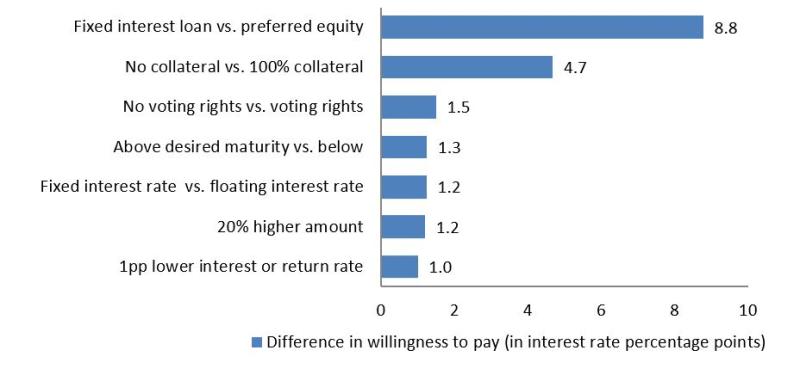

The results were staggering. The premium on debt financing interest rates that companies were willing to take in order to avoid external equity financing that included voting rights was 880 basis points. Essentially, firms were willing to pay an extra 8.8% interest compared to the cost of equity so they wouldn’t have to offer shares. Even with a lending option requiring 100% collateral, firms were willing to pay some 5% more for a loan.

How much extra are firms willing to pay for different financing characteristics?

Why is this bad for Europe? Because it creates staggering costs for society. Here’s what our studies found:

- Firms that were more leveraged before the financial crisis had it tougher in the lean years, and will have it tougher when the next crisis comes around;

- Bank debt is not suited to finance intangible investment and innovation. Banks like collateral. They are not keen to provide debt financing for the acquisition of the intangible assets that are so important to innovation. Our analysis shows that firms with more diversified financing (e.g. trade credit, bank financing, grants and equity financing) invest more in intangibles and in innovation;

- Innovation is also about taking risks, which is why equity finance is so important, and why debt, which needs stable returns, isn’t so good. Our analysis also shows that Europe lags behind the US when it comes to leading innovators, particularly among small and young firms. Less effective growth finance might be one of the causes.

So in practice, does bank debt just feel right?

In our experiment, firms picked the debt offer in 80% of all presented options. The experiment, detailed in the European Investment Bank’s annual Investment Report, helps explain the large share of debt financing in Europe, also by pointing to a lack of demand for equity.

This aversion to equity financing was not explained by any other variable that we controlled for. It cannot easily be explained by economic theories. But we have some ideas about what can be done to improve the situation.

What can be done?

First, European regulators should level the playing field for equity financing. Interest rates on debt financing are usually tax deductible. Profits are taxed, and so are dividends on equity.

Second, we need to move forward with the Capital Markets Union to create a true single market and a cross-border European market. In this, we especially need to prioritise private equity and venture capital investment. Extensive bank financing is currently crowding out equity financing – and in the process, crowding out companies that would benefit from more equity financing. Naturally, public listings for equity are important as well, but less practical for smaller firms, which are slightly more enthusiastic towards equity financing.

Only if these measures are taken will firms change their approach. That’s the best way forward for European innovation finance.