Our Economics department keeps track of all the important developments in the financial markets in both advanced economies and emerging markets. We are publishing periodic briefings with analytical assessments of the current macroeconomic and financial market situation. Find out more about the EIB Group's response to the crisis

Overview

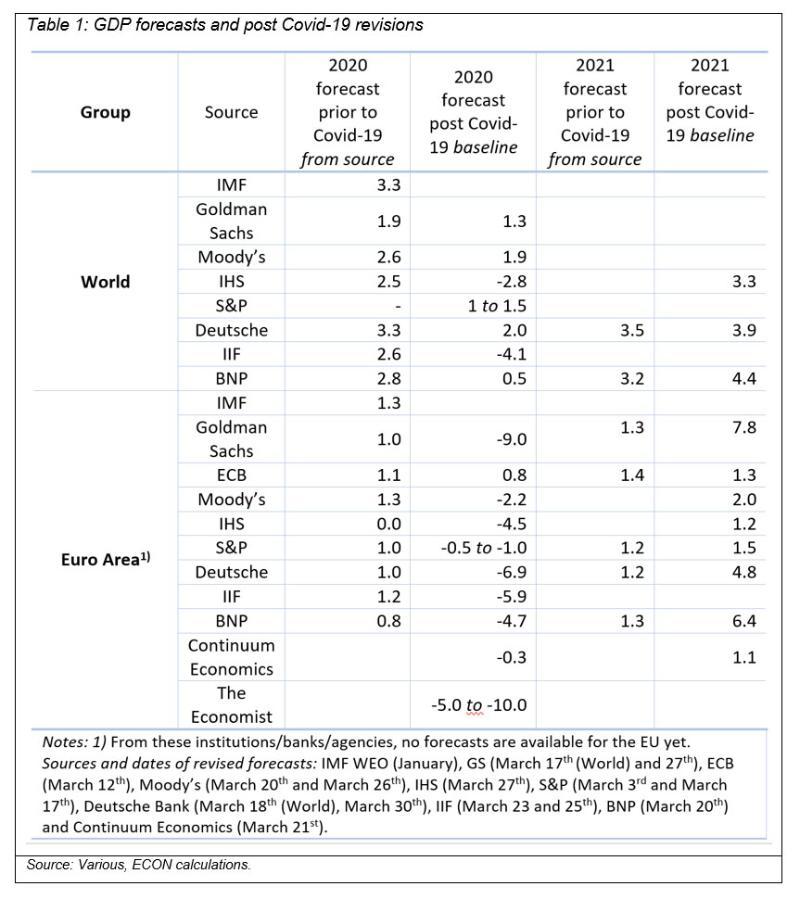

- The first releases of hard and soft economic indicators for the world and the EU economy are extremely pessimistic. Some economic sentiment and consumer confidence indicators are approaching the lowest levels ever observed and point to a severe contraction of economic activity. This could reach anywhere between -5% and -10% or more in the euro area in 2020 according to the latest forecasts (Section 1). As the crisis unfolds, it is clear that the unemployment and debt levels in Europe will remain elevated for some time.

- To counteract this unprecedented shock, policymakers are implementing new measures at the national and supra-national level (Section 2). In the EU, the amount of fiscal measures at national level has reached about 2% of GDP mid-last week, doubling within seven days and still increasing in size albeit with significant differences across Member States. Support schemes for firms and workers have been shored up and additional direct support for hospitals and the health sector is foreseen in some cases (for example, Italy, Lithuania and Germany). Member States have put in place additional measures to mitigate the social hardship resulting from the temporary drop in income. This includes support for parents staying home (Romania), expanded unemployment benefits (Malta) and possibilities to defer rent or mortgage payments and steps to support entrepreneurs and the self-employed, including in France and Germany. Credit guarantees for firms by Member States are also substantial (estimated to exceed 10% of GDP, for instance, in the Czech Republic, France and Germany). The US approved an economic support package worth USD 2 trillion (about 9% of GDP). This is twice as big as the package implemented in response to the global financial crisis in 2008-09.

- At the EU level, flexibility via the Stability and Growth Pact was granted, and new policies are currently being discussed. Those include a proposal for the European Stability Mechanism (ESM) to develop a precautionary facility with/without reduced conditionality using the ESM’s existing financial resources (Section 3) and a proposal by the EIB to go beyond its initial up to EUR 40 billion COVID-19 economic response package. A decision on further measures at EU level to tackle the socio-economic consequences is still pending and the European Council asked the Eurogroup to present proposals within the next two weeks. A timely and sizable response - targeting the sectors of the EU economy that are being most hardly hit (households, services, micro, small and medium enterprises) - is of paramount importance: hardship is being felt across the more vulnerable segments of the population and may soon give rise to bouts of social discontent.

- Across the globe, financial conditions remain tight and some sovereigns (most notably the UK) and corporates have had their ratings downgraded (Section 3). Equity markets in advanced and emerging economies recovered somewhat, but volatility remains elevated. Markets show that banks might also experience some funding difficulties, although quite different in nature from those observed during the 2008-2009 global recession. Banks being the key external funding source for SMEs, the backbone of the EU economy, they also need to be safeguarded.

- This note also contains a preliminary analysis of the economic impact of COVID-19 outside the EU and identifies the main channels of transmission of the crisis (Section 4), including direct impacts of lockdowns; disruption in via global value chains; drop in global demand for commodities and tourism; contraction remittance inflows and access to international finance; and stress on vulnerable sovereigns.

1. Evolution of the COVID-19 pandemic and expected impact

As of 30 March, since the start of the pandemic there have been about 750,000 infections, more than 35,000 people have died, while more than 150,000 people have recovered from COVID-19. The US became the epicentre of the virus (Figure 1), with Italy having the heaviest death toll in the world (over 11,000 people) and Spain is fast approaching. The latest official data on mortality shows that the elderly and people suffering from a combination of chronic diseases, including cardiovascular problems, diabetes, respiratory problems and cancer, are disproportionally more affected and vulnerable, keeping in mind that social responsibility to contain the spread of the virus goes well beyond these vulnerable groups.

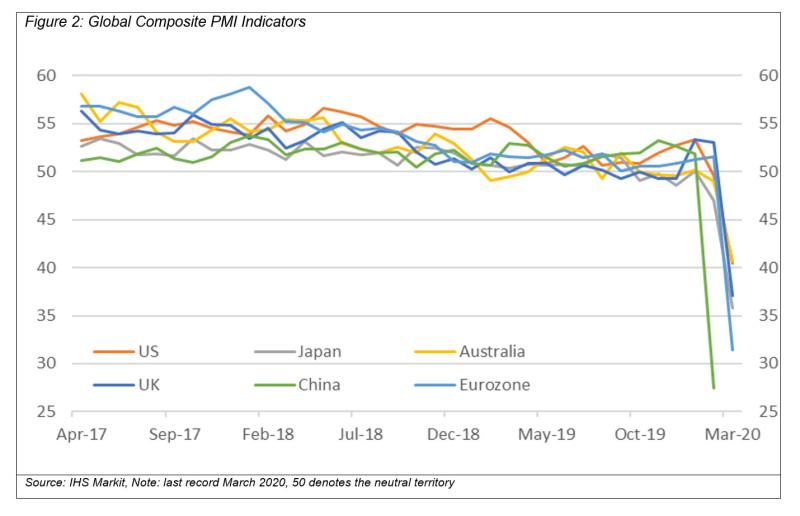

Business and consumer confidence indicators plummeted across the globe in March, with some subcomponents reaching all-time lows. Flash global Composite PMIs (Purchasing Managers' Index) in March declined sustainably (Figure 2). In France, the business climate indicator has experienced its most significant drop since the start of the series (1980). A similar dynamic was also observed in Italy where both consumer sentiment and economic climate indicators have plummeted sustainably. In Germany, the IFO Export Expectations in manufacturing decreased from -1.1 points to -19.8 points, its lowest level since May 2009, marking the sharpest drop since German reunification.

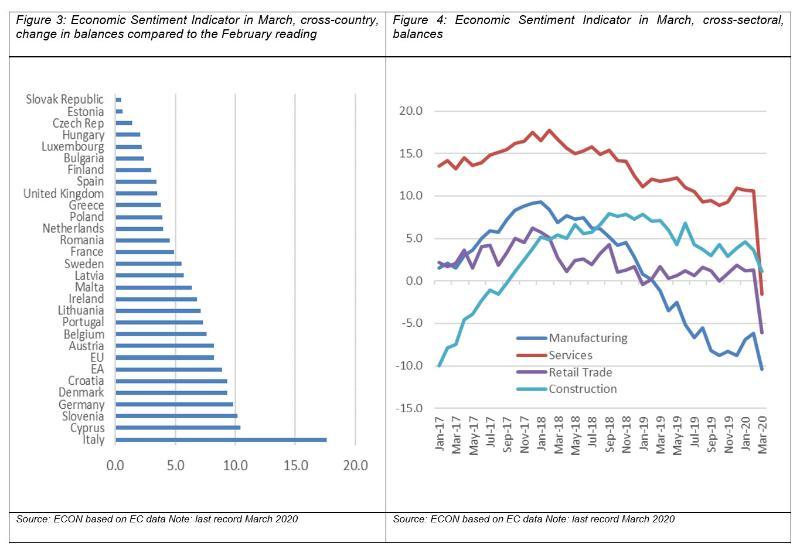

The Economic Sentiment survey for the EU published today also shows a sharp decline. Economic Sentiment indicators fell dramatically in both the euro area (-8.9 points down to 94.5) and the EU (-8.2 down to 94.8 points). Similarly, the Employment Expectations Indicator (EEI) plummeted by 10.9 points to 94.1 in the euro area and by 9.7 points to 94.8 in the EU. This is the single worst monthly fall since the series started in 1985 and is at the lowest level since 2013. Italy experienced the biggest decline in sentiment, with a drop of 17.6 points, followed by Cyprus, Slovenia and Germany (Figure 3). By sectors (Figure 4), services experienced the steepest decline (from 10.6 to -1.6) followed by retail trade (from 1.3 to -6.1). At a more disaggregated level, accommodation, food and beverage are the most hit among the services and clothing, leather and furniture among the manufacturing.

Incoming macroeconomic data clearly point to a severe recession. In the US, weekly jobless claims increased to 3.2 million in the week to 26th March, from 282,000 the week before. Economic growth in Singapore tumbled by an annualised 10.6% in Q1 2020, the sharpest drop in a decade, showing that even the countries that have been most effective at fighting the disease can expect to contract substantially.

Despite the encompassing nature of the shock, some sectors will experience relatively sharper contractions. The tourism sector, one of the most strongly hit, will face an output decrease as high as 70% in some countries as reported by the OECD. The airline industry also faces rather grim prospects. The International Air Transport Association (IATA) reports that 1.1 million flights have been cancelled as of March 27th and year-on-year bookings are down about 50% in March and April and by 40% for May. Up to now, around one-third of the total global passenger fleet has been parked. IATA also estimates that passenger revenues will be USD 252 billion lower this year compared to 2019 and that revenue passenger kilometre, one of the key measures for the passenger traffic profitability, will decline by 38% in year-on-year terms, assuming about a three-month deadlock. Another badly hit sector is the automotive industry. According to preliminary simulations by IHS Markit, the German automotive sector could shrink anywhere between 9.6% and 30.6%, while the wholesale trade could contract between 6.5% and 7.5%. In Italy, the sharpest contraction is expected in the accommodation and tourism sector, ranging between -4.4% to -22.4%, while machinery and equipment sector could contract by above 10%. In France, the accommodation and tourism sector could shrink between 0.7% and 12.7% this year. In Spain, the automotive sector could decline between 4.7% and 35.7%, while accommodation and tourism could drop between 1.8% and 9.8%.1

1) Simulations were run on latest PMI sectoral data and latest available IHS forecast.

In line with the sobering data releases, 2020 real GDP forecasts are being constantly revised downwards. A severe global recession, with a contraction of economic activity stronger than during the 2008-2009 financial crisis, is now the most likely baseline scenario according to most recently published projections. Indeed, the Economist expects the US and the euro area GDP to contract between 5 and 10% this year and potentially more in a more adverse scenario. The OECD has also estimated that for each month of containment, a loss of 2 p.p. points in annual gross domestic product can be expected. Therefore, if the shutdown continues for three months, as currently envisaged by most observers, with no offsetting factors, annual GDP growth could be 4 to 6 p.p. lower than originally forecast. Having said this, extreme uncertainty continues to surround these figures as few hard data are available so far in the year, and it remains difficult to predict for how long drastic containment measures will remain in place.

2. Policy response

Policymakers around the world have responded with further actions to counter the dramatic economic fallout of the COVID-19 pandemic. The single most important response came from the United States where the Senate unanimously passed a USD 2 trillion (about 9% of US GDP) economic support package on Wednesday, March 25th. The size of the package is unprecedented in US history. Its components include an envelope of USD 250 billion for payments to individuals of about USD 1,500 per adult. USD 250 billion is set aside to expand the unemployment coverage, including support for freelancers. The bill also establishes a USD 100 billion public health and social emergency fund to reimburse providers for expenses and lost revenues. To support distressed businesses, a loan and guarantee package is also included in the bill, including USD 350 billion in small business loans, and USD 500 billion in loans for distressed companies. Student loan repayments are also to be suspended.

EU Member States have also put forward a set of response measures to the pandemic. The amount of fiscal measures at national level has reached about 2% of GDP mid-last week, that is twice the size compared to only about a week ago and is increasing in size. Fiscal stimulus and other support measures vary in size across Member States and in terms of the specific instruments deployed, also reflecting domestic circumstances1, with additional direct support to hospitals and the health sector (e.g. Italy, Germany) and support schemes for firms and workers shored up. Notably, Member States have put in place additional measures to mitigate social hardship resulting from the temporary drop in incomes and to support entrepreneurs and self-employed (e.g. France and Germany).

At the EU level, a number of measures have been discussed. Proposals are currently focusing on the possibility for euro area countries to expand their room for fiscal manoeuvre through some form of risk-sharing. These would come on top of steps already taken so far, which include the application of full flexibility of the EU fiscal rules and the revised State Aid rules, increasing leeway for Member States’ policy action, and common support via the EUR 37 billion Coronavirus Response Investment Initiative (CRII) to support small businesses and the health care sector. Moreover, the European Central Bank's (ECB) EUR 750 billion Pandemic Emergency Purchase Programme (PEPP) is a major step to provide relief via monetary policy action.

The proposal of the EIB to set up a EUR 25 billion pan-European guarantee fund with contributions from Member States to boost support for firms in the EU has also been discussed at Ecofin and Eurogroup levels. The fund could build on the EIB Group’s already existing guarantee programmes and pan-European deployment channels, and therefore be deployed within a very short timeframe.

The European Commission also indicated that it is considering additional measures. Commission President Ursula von der Leyen issued a statement over the weekend (March 28th) indicating that the Commission will participate in these discussions and stands ready to assist.2 In parallel, the Commission is working on proposals for the recovery phase within the existing treaties, such as full flexibility of existing funds - such as the structural funds. The Commission will also propose changes to the MFF proposal and include a stimulus package that will ensure that cohesion within the Union is maintained through solidarity and responsibility. The President stated that she is not excluding any options within the limits of the Treaties.

1) Including NPB involvement and social support systems.

2) See link: https://ec.europa.eu/commission/presscorner/detail/en/STATEMENT_20_554

3. Financial markets

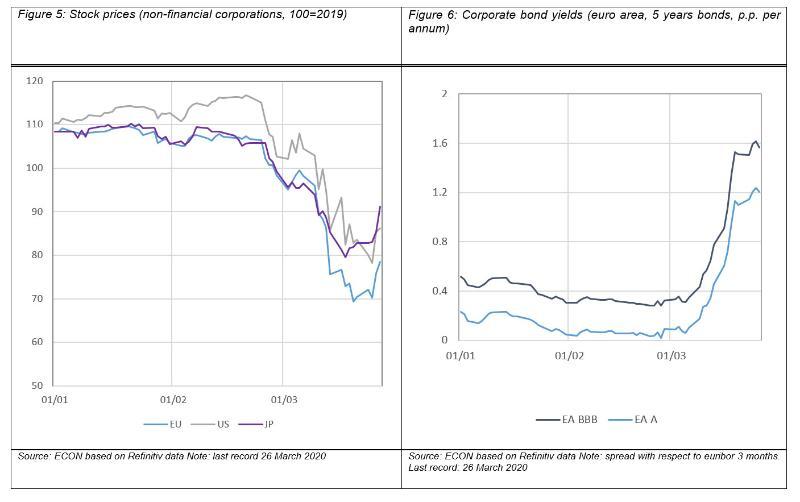

Stock prices rebounded substantially. The rebound, of around 10% on a weekly basis, was comparable across the main developed economies, the US, EU and Japan (Figure 5). In Europe, around one-third of the fall recorded since the beginning of the crisis has been recovered, with stocks remaining 20% below their level in 2019 to date. The rally reflects a positive reaction to the policy measures announced this week, particularly the US package and the G7 Statement emphasising the commitment to collective and coordinated actions.

Corporate bond yields have plateaued in Europe. The continuous, substantial rise that has been observed since the beginning of March, from 0-40 to 120-160 bps for corporates rated A to BB and bonds of 5-years maturity, has been suspended (Figure 6). Currently, corporate bonds spreads stand well less than half-way from the peak reached during the Lehman crisis, at the beginning of 2009. The rise in corporate bond yields has been symmetric across the rating spectrum. Indeed, at the current juncture, the sectoral dimension may dominate considerations usually brought forward to estimate risk: passenger airlines, tourism, automobile, hotels and restaurants and non-food retail sector are the most exposed, while pharmaceuticals, utilities, energy and digital are cushioned. This is reflected in the wave of downgrades implemented by rating agencies in the previous week.

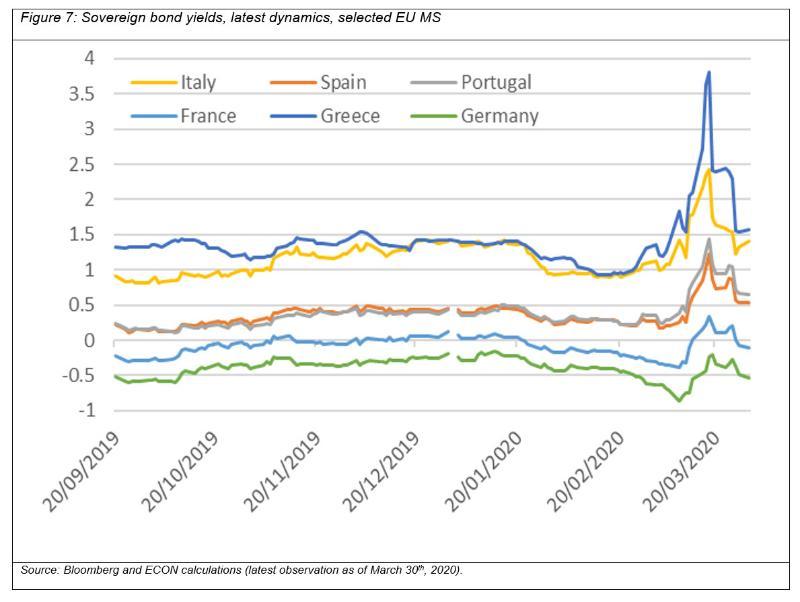

Sovereign bond yields were much less volatile last week, and, when moving, tended to fall. Cyprus, Greece, Italy, Portugal and Spain experienced a large decline on Thursday (Figure 7), when the ECB declared that it would scrap its self-imposed bond-buying limit of a third of a member state’s debt. The compression of bond yields stretched beyond the euro area, with the Czech Republic, Hungary, Poland and Romania also experiencing a drop in yields. Outside the EU, the UK was downgraded by Fitch to AA- with a negative outlook.

Funding markets for banks are showing some signs of distress, but the current situation is different from the global financial crisis. In 2008/2009, banks faced real liquidity constraints that are now almost residual, given the central banks' long-term liquidity provision. Money market spreads, usually a measure of liquidity risks, show some stress in the US. The Libor-OIS spread increased by almost 100bps in March, the steepest increase since the global financial crisis. This likely reflects the increasing demand for USD, the global funding currency. Indeed, heightened uncertainty pushes up demand for USD funding worldwide. Some global banks have opted for issuing long-term debt despite the recent increase in funding costs. That said, the current Libor-OIS spread is quite far from the peak levels registered during the global financial crisis. Additionally, in the euro area, the euribor-eonia spread barely increased since the start of the COVID-19 crisis.

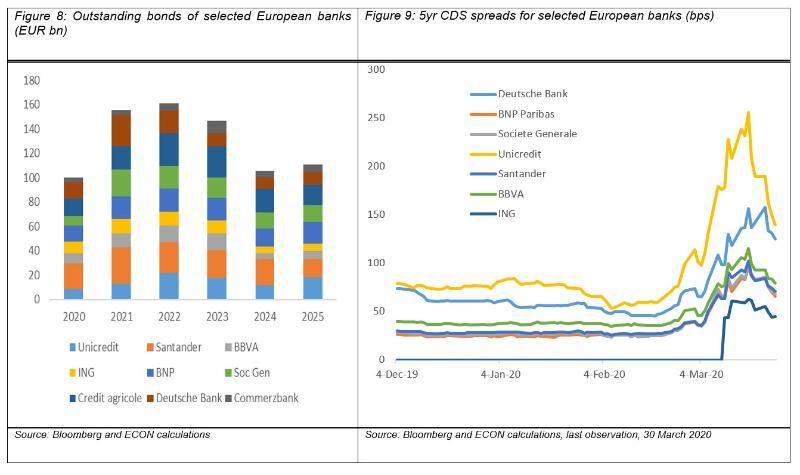

While the funding provided by the central banks virtually eliminates the risk of a severe liquidity crisis, this does not mean that all banking sectors and banks face the same challenges. Funding needs from maturing bonds for the main European banks will reach close to EUR 800bn until 2025 (Figure 8). The bulk of these needs are concentrated in 2021 and 2022, when maturing debt will reach EUR 320bn for the group of selected banks. Some banks show a relatively smooth maturities profile while others have most of their funding needs concentrated until 2022.

After a sharp increase in the beginning of the month, European Financial institutions credit risk came down somewhat during the week. CDS spreads, increased substantially since late February but registered a relative decline in the past week. The picture is relatively common across some of the main European Banks. Still, banks show a different credit risk depending on the country where they concentrate their operations and their idiosyncratic profiles (Figure 9).

4. Non-EU economies - a preliminary assessment

Non-EU economies are also likely to experience a painful shock. Several non-EU countries are already reporting a large number of cases, with Iran, South Korea, Turkey and Brazil reporting the largest numbers. Case numbers are significantly lower elsewhere, including in most African countries. However, cases may be underestimated, due to limited capacity for testing, and the epidemic is expected to accelerate across the globe. The ability of health systems to cope varies widely. In many countries, health systems are extremely weak, particularly in low-income countries. If infections take off, as sadly seems likely, the human impact could be devastating, in the poorest countries in particular. There is a risk that the crisis, exacerbating existing fragilities, could lead to social unrest and a deterioration in security, particularly in countries that are already fragile or conflict-affected.

Six main economic transmission channels can be identified for these countries:

- Direct impacts of lockdowns, travel restrictions and border closures, as well as higher rates of morbidity and mortality. Most countries are in the process of imposing lockdowns, border closures and other restrictions, which are slowing economic activity. Demand is plunging, production is disrupted and investment plans are being put on hold. Lockdowns are hurting labour-intense service sectors, affecting in particular countries where unemployment is already high.

- Decline in commodity prices (e.g. oil, gas, copper and iron) triggered by the economic slowdown in virus-affected countries and the oil price war. According to IHS, the oil price slide will depress economic activity by almost 1% of GDP in Mexico, Brazil and Colombia. In Ecuador oil contributes 10% of GDP, and oil revenues are now forecast at USD 3.2b in 2020, compared to over USD8b in 2019. In Sub-Saharan Africa (SSA), the major oil exporters, such as Nigeria and Angola are highly exposed. Some of the poorest countries in the world, such as Sierra Leone, Liberia, Democratic Republi of the Congo and Zambia will also be impacted by falling prices of iron ore and copper. The sharp decline in oil and commodity prices adds a strain also on commodity exporters in the EU Southern and Eastern Neighbourhood, (e.g. Algeria, Azerbaijan, Kazakhstan, Russia, Uzbekistan and Ukraine as transit, Belarus as transit and oil refining).

- Disruption to global supply chains and demand for manufactured goods from countries impacted by COVID-19. Latin America (LATAM) is highly exposed, as 43% and 12% of exports are to the USA and China, respectively. Supply chain disruptions are going to be heavily felt in Asia: shortages in textile supply from China are leaving hundreds of thousands workers unemployed in Cambodia and Bangladesh for instance. Manufacturing is of relatively limited importance for SSA as a whole, but countries such as South Africa will be badly impacted and the breakdown of supply chains may make it difficult for countries to access food and essential medical supplies. SSA is the region most reliant on food imports in the world, and all countries are net importers of medical supplies. LATAM is heavily dependent on imports from the US. The relatively high level of trade integration of the Western Balkans with the EU, in particular with Italy and Germany, has resulted in a halt of industrial production in the region. Good exports from the Eastern Neighbourhood are also highly dependent on European and Russian demand, so these countries will be heavily impacted, including for instance Ukraine (highly reliant on manufacturing), Uzbekistan (one of the largest producers of cotton) and Belarus (e.g. oil refineries and potash).

- Disruption to tourism and remittance flows. Several island states and a number of other economies will be badly hit by a decline in tourism, while many countries are vulnerable to a decline in remittances. The current account of oil importers (e.g. Armenia, Georgia, Jordan, Moldova, Morocco, and Tunisia) and all Western Balkan countries will be affected by lower remittance inflows and weaker demand for goods and services, including tourism (e.g. Egypt, Georgia, Armenia, Moldova, Montenegro and Albania). Twelve countries in SSA are particularly exposed to the impacts on tourism, with tourism revenues accounting for over 10% of GDP –Seychelles, Cape Verde and Mauritius are the most affected. Six SSA economies will be particularly impacted by a drop in remittances, as these account for over 10% of their GDP. Of these, five are also among those most affected by a drop in tourism revenues. South-East Asia and the Caribbean are also particularly exposed to a drop in tourism and remittances.

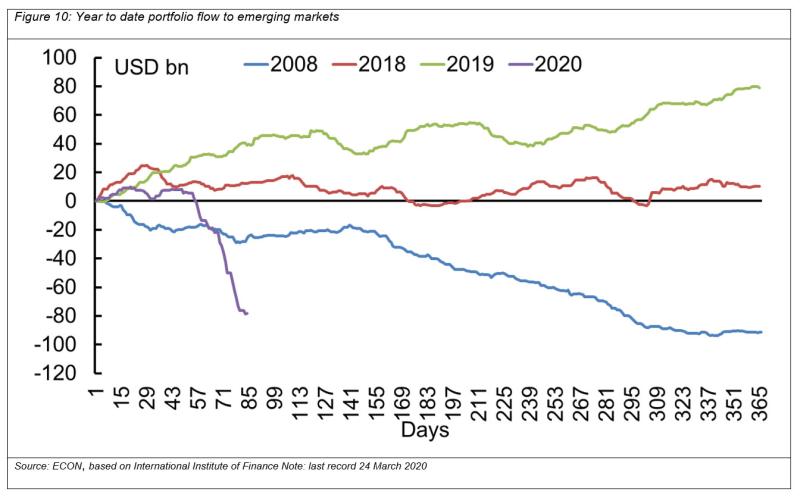

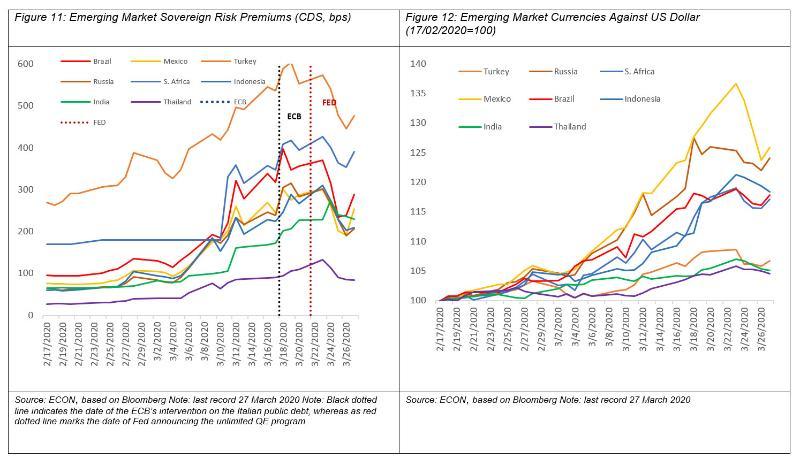

- Heightened risk aversion and flight to quality, resulting in plummeting capital inflows. Since early March, flight to quality has led to a sharp reversal in portfolio flows, thus contributing to a surge in government bond spreads, collapsing equity prices and significant domestic currency depreciations. As of March 24th, total capital outflows from emerging markets reached USD 78 billion (this compares with a total outflow of about USD 90 billion in the entire course of 2008 - Figure 10). Spreads on emerging market bonds have already increased sharply, indicating significant liquidity tensions, which if protracted may lead to sustainability problems. These developments are particularly worrisome for small frontier and emerging market economies, but also for large countries heavily reliant on foreign funding like Turkey, South Africa, Nigeria, India, Ukraine, and Indonesia (Figure 11). South Africa was downgraded by Moody's to Ba1 from Baa3 and outlook remains negative. Bond yields increased rapidly for SSA countries from mid-March. Yields on Zambia’s bonds have risen to around 50%. In the last month, Argentina’s USD denominated bonds increased by 2100 basis points, whereas Brazil, Mexico and Chile experienced a 200 basis points increase. Steep depreciation trends in EM currencies, resulting from massive capital outflows, also threaten macroeconomic (e.g. through increasing inflationary pressures) and financial stability (e.g. increased dollarisation, rollover and repayment capacity) in these countries. The Mexican peso and the Brazilian real depreciated heavily, by 31% and 15% respectively in the last month (Figure 12). Several SSA oil exporters have seen major depreciation. Nigeria was forced, by rapid loss of reserves, to unify its multiple exchange rates – equivalent to a devaluation of around 17%. In addition, retrenchment in remittances will harm many Eastern Neighbouring countries heavily dependent on them to sustain the national income and using them as a source of foreign currency financing. For less developed emerging markets, typically heavily reliant on bilateral and multilateral loans to cover for external financing needs, lender counterparties’ ability and willingness to roll over maturing debt will be critical. Among those, countries that are more reliant on IFIs’ funding are likely to experience less stress.

- Deterioration of fiscal balances and increased costs of external financing, pushing up risks of sovereign downgrades and defaults. Countries with large external debt burdens, such as South Africa, Zambia, Angola, Montenegro and Albania are particularly vulnerable. Economies that are highly dependent on oil for foreign exchange, such as Nigeria and Ecuador, or closely linked to virus-hit countries (for instance Mexico), economies in extreme economic difficulties, such as Lebanon, Argentina and Zimbabwe and those recovering from extended slumps, for example Mozambique, are also poorly placed to deal with the severe tightening of global financial conditions. The World Bank and the IMF have expressed support for debt relief for the poorest countries.

Room for policy response is limited and support from the international community will be needed as much as ever. In many emerging and developing countries the room for manoeuvre to counteract the economic downturn is going to be hindered by already weak macro-financial conditions, limited fiscal space and constrained access to international finance (market or otherwise). Some countries, such as Nigeria, have or will be forced to adjust their 2020 budgets downwards to account for loss of revenues from commodities. A number of countries have cut monetary policy rates, and a number of central banks are providing payment holidays on facilities to commercial banks, introducing new liquidity facilities, or extending eligibility for existing facilities to critical centres such as healthcare. Some are mandating or “requesting” commercial banks to provide payment holidays to their creditors, particularly the poor and micro, small and medium enterprises (MSMEs). A number of central banks are temporarily reducing reserve requirements or exercising varying types of forbearance on commercial banks, in an attempt to keep money flowing in the real economy. Despite these interventions, for many of these countries the trade-off between containment measures to stop the virus from spreading and the economic contraction that they will bring poses an even more daunting challenge than in the advanced economies and it will require as much support as possible from the international community.

5. Conclusions

The world economy is faced with an unprecedented shock and strong policy responses are being taken. While forecasts remain ‘work in progress,’ a global recession is on the cards according to all analysts and commentators. The size can be expected to be comparable or even higher than the 2008-09 global financial crisis, the duration is still highly uncertain, but unprecedented policy response also gives some comfort for a recovery. Yet, the long-term effects of COVID-19 are not to be underestimated. This holds particularly true for the EU, where multiple spillovers between the real economy and financial markets and feedback loops between corporates and banks on the one side, and banks and sovereigns on the other, are very real, as already witnessed during the sovereign debt crisis. To contain the economic fallout, national and EU-wide responses need to be credible, coordinated and fast. They also need to target the hardest hit segments of the economy.

The capacity of health systems needs to be addressed as a priority as this has reached the limits in the most exposed countries. Direct support to firms developing vaccination and treatments and financial aid to hospitals should be put very high on policy agendas. The SME sector, the backbone of the EU economy for employment creation, will suffer disproportionally and therefore, measures to protect jobs and production capacity need to be drastic. These can take a form of direct financial support, guarantees, tax reliefs, measures to prevent large scale lay-offs etc.

|

Country |

Source |

2020 forecast prior to COVID-19 from source |

2020 forecast post COVID-19 baseline |

2021 forecast prior to COVID-19 from source |

2021 forecast post COVID-19 baseline |

|

Italy

|

IMF |

0.5 |

|

|

|

|

Goldman Sachs |

0.2 |

-3.4 |

|

|

|

|

IHS |

-0.1 |

-3.5 |

|

|

|

|

S&P |

0.2 |

-11.6 |

0.6 |

1.0 |

|

|

Deutsche |

0.5 |

-2.7 |

0.6 |

2.6 |

|

|

Continuum Economics |

- |

-1.7 |

|

0.8 |

|

|

Moody’s |

|

-2.7 |

|

2.1 |

|

|

Prometeia |

0.1 |

-6.5 |

|

|

|

|

Germany |

IMF |

1.1 |

- |

|

|

|

Goldman Sachs |

0.9 |

-8.9 |

1.4 |

8.5 |

|

|

IHS |

0.4 |

-1.2 |

|

|

|

|

S&P |

0.5 |

0.0 |

1.0 |

1.5 |

|

|

Deutsche |

1.0 |

-4.5 |

1.1 |

3.4 |

|

|

Continuum Economics |

- |

-0.3 |

|

1.1 |

|

|

Moody’s |

|

-3.0 |

|

2.5 |

|

|

German Council |

|

-2.8 |

|

3.7 |

|

|

France |

IMF |

1.3 |

- |

|

|

|

Goldman Sachs |

1.1 |

-7.4 |

1.4 |

6.4 |

|

|

IHS |

0.8 |

-0.6 |

|

|

|

|

S&P |

1.3 |

0.7 |

1.3 |

1.7 |

|

|

Continuum Economics |

- |

0.0 |

- |

0.9 |

|

|

Moody’s |

|

-1.4 |

|

1.8 |

|

|

Spain |

IMF |

1.6 |

- |

|

|

|

Goldman Sachs |

1.8 |

-9.7 |

1.7 |

8.5 |

|

|

IHS |

1.7 |

-1.8 |

|

|

|

|

S&P |

1.7 |

1.3 |

1.6 |

1.9 |

|

|

Continuum Economics |

- |

-0.2 |

|

0.8 |

|

|

Portugal |

BdP |

1.7 |

-3.7 |

1.6 |

0.7 |

|

Czeck Republic |

IIF |

2.6 |

-5.4 |

|

|

|

BNP |

2.7 |

-1.0 |

3.0 |

7.0 |

|

|

Hungary |

IIF |

3.0 |

-6.0 |

|

|

|

BNP |

3.1 |

-1.5 |

3.6 |

6.0 |

|

|

Poland |

IIF |

3.9 |

-6.4 |

|

|

|

BNP |

3.3 |

0.5 |

3.4 |

6.0 |

|

|

Romania |

IIF |

3.4 |

-6.1 |

|

|

|

BNP |

3.0 |

-2.0 |

3.5 |

7.0 |

|

|

Slovenia |

MIoS |

1.5 |

-6.0 |

2.2 |

|

|

UK |

Moody’s |

|

-2.6 |

|

2.4 |

|

Goldman Sachs |

1.0 |

-7.5 |

2.1 |

7.3 |

|

|

IHS |

|

-4.3 |

|

0.8 |

|

|

China |

IMF |

6 |

- |

|

|

|

Goldman Sachs |

5.5 |

3.0 |

|

|

|

|

Moody’s |

6.2 |

3.3 |

|

6.0 |

|

|

IHS |

5.8 |

2.0 |

|

6.4 |

|

|

S&P |

- |

2.7 to 3.2 |

|

|

|

|

Deutsche |

6.1 |

1.0 |

6.0 |

10.0 |

|

|

IIF |

5.8 |

2.8 |

|

|

|

|

BNP |

5.7 |

2.6 |

5.8 |

7.6 |

|

|

Continuum Economics |

- |

5.3 |

|

6.0 |

|

|

US |

IIF |

1.5 |

-4.9 |

|

|

|

Goldman Sachs |

2.3 |

-3.8 |

2.4 |

5.3 |

|

|

Continuum Economics |

|

-0.7 |

|

2.9 |

|

|

BNP |

1.5 |

-0.7 |

2 |

2.4 |

|

|

Moody’s |

1.8 |

-2.0 |

|

2.3 |

|

|

Deutsche |

1.9 |

-0.8 |

2.1 |

2.4 |

|

|

S&P |

1.9 |

1.6 |

|

|

|

|

The Economist |

|

-5.0 to -10.0 |

|

3.4 |

|

|

IHS |

|

-5.4 |

|

|

Notes: 1) From these institutions/banks/agencies, no forecasts are available for the EU yet.

Sources and dates of revised forecasts: IMF WEO (January), GS (March 17th (World) and 27th), OECD (March 27nd), ECB (March 12th), Moody’s (March 20th and March 26th), IHS (March 27h), S&P (March 3rd and March 17th), Deutsche Bank (March 18th), IIF (March 23 and 25th), BNP (March 20th), Continuum Economics (March 21st) , The Economist (March 28th).