Our Economics department keeps track of all the important developments in the financial markets in both advanced economies and emerging markets. We are publishing periodic briefings with analytical assessments of the current macroeconomic and financial market situation. Find out more about the EIB Group's response to the crisis

Overview

- Economic sentiment indicators released in the course of the week ending April 3, 2020 added further gloom to the economic outlook for the European Union and the rest of the world. Jobless claims have skyrocketed in the United States and came well above expectations. In some EU countries, initial labour market data is also worrisome (e.g. Spain, France, Italy, Germany). In 2020, economic activity is expected to contract between 5% and 10% in the Euro area, while some EU countries could experience an even sharper contraction. All sectors, especially services, retail trade and manufacturing, will be extremely hit in the following months (Section 1).

- At the national level, additional economic measures to counter the crisis have been taken. Support schemes are now moving into the implementation phase in a number of countries. The size of the policy intervention differs sustainably across EU countries, ranging between 1% of GDP and over 20% of GDP. At the EU level, The European Commission presented a proposal for temporary support to mitigate unemployment risk in an emergency, designed to help protect jobs and workers affected by the coronavirus pandemic. Furthermore, the Eurogroup continues preparatory work on proposals to develop pan-European financial responses, to be discussed on April 7. The importance of a pan-European scheme is evident in the context of a highly integrated European economy, where spillovers, related to intra-EU trade, European confidence and financial loops are sizable for each and every member state (Section 2).

- Financial conditions remain tight and stock markets volatile in both advanced and emerging economies (EM) (Section 3). Although relatively high, European sovereign and corporate spreads remained mostly stable this week. Further, bond issuance was strong among investment-grade corporates. On the other hand, capital outflows from emerging economies have reached a record USD 83.3 billion on a cumulative basis since the beginning of the year, and several developing and emerging countries have seen their sovereign ratings downgraded. Going forward, heightened financial market volatility is to be expected.

- Zooming in on European banks (Section 4), the banking sector is in a better shape than during the 2008-2009 financial crisis, but clearly the current economic shock poses risks. In comparison to the 2008-2009 financial crisis, the initial shock will most likely be shorter if the policy response remains strong, timely and well-targeted; the the crisis is not originating in the financial and banking sector; and banks have sounder capital and liquidity positions than in 2008 on the back of the policy and regulatory measures undertaken following the financial crisis. On the other hand, the contraction in GDP is likely to be more substantial and more concentrated in time than during the global financial crisis. It is also likely to trigger a more immediate impact on non-performing loans, as entire economies are being shut down. All in all, we expect European banks to remain resilient. Yet, uncertainty remains huge and a prolonged or sharper recession will not leave banks unscathed.

1. Evolution on the COVID-19 pandemic and expected economic impact

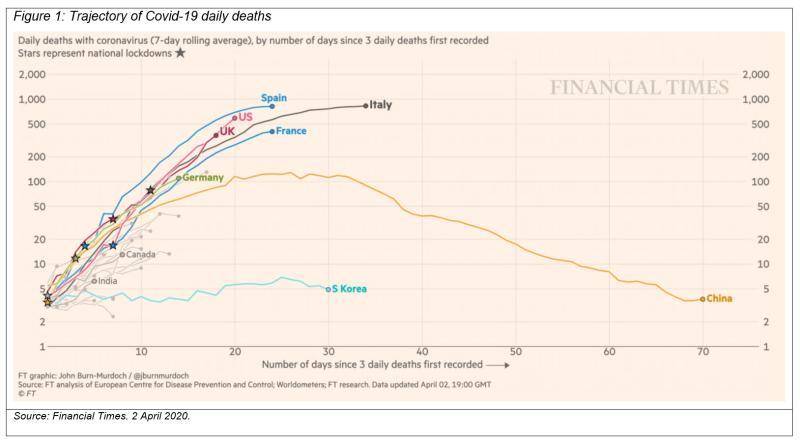

As of 3 April, more than 1,000,000 infections have now been confirmed and more than 50,000 people have died due to the virus or by the complications it caused. More than 200,000 patients have recovered. The epicentre of the virus has moved to the United States, where new infections are increasing exponentially. While at the moment the heaviest death toll remains in the European Union (Figure 1), infections seem to have plateaued in Italy and Spain (the most affected countries in Europe so far).

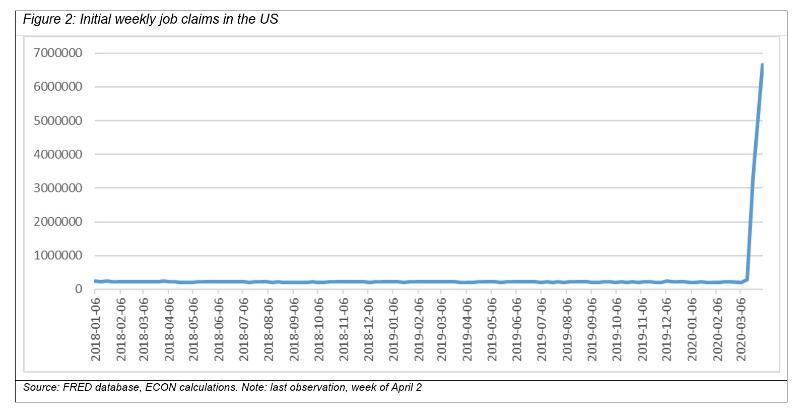

Economic data continue to point to a sharp contraction of global economic activity. The weekly initial jobless claims in the US, a forward-looking measure of unemployment, continued to rise up to April 2, with the number of first-time unemployment benefits seekers hitting an all-time high of 6.65 million (it was 3.3 last week – Figure 2). Further, the US economy shed more than 700,000 jobs in early March and the unemployment jumped to 4.4%, the highest in more than two-and-a-half-years. In France, a fifth of all private sector employees in 400,000 companies are seeking temporary unemployment benefits, with 4 million people taking up a government support scheme according to the data published yesterday. In Spain, the number of people filing for jobless claims rose to a record high of 302,000 (not seasonally adjusted), while employment (adjusted for seasonality) actually declined by more than 400,000 jobs. In addition, the final March PMI in the euro area was even lower than the flash one. The composite indicator, which includes services and manufacturing, fell to 26.4, down from 52.6 in February. The decline was broad-based across Europe and, based on currently available forecasts, the contraction of economic activity could reach between 5 and 10% in the euro area (Table 1) and potentially even more in case drastic containment measures persist for a longer time. On a positive note, China’s Manufacturing PMI surged to 52.0 in March from a record low of 35.7 in the previous month.

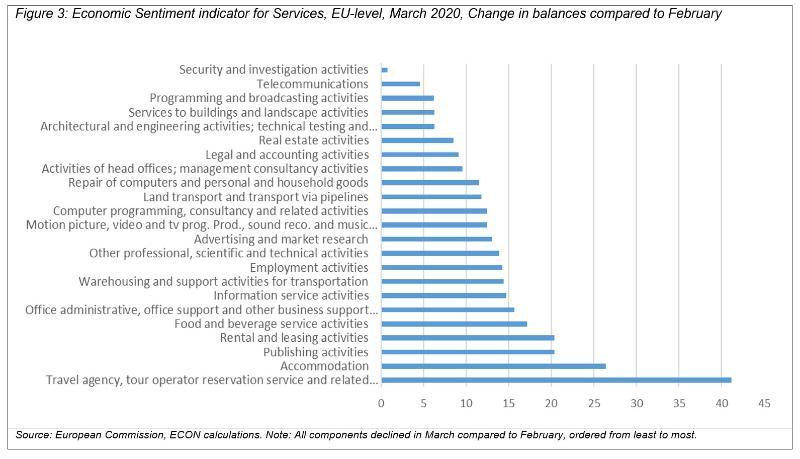

The services sector - where a significant share of SMEs operates - will be hit particularly hard, as shown by the Sentiment indicator compiled by the European Commission. Indeed, services experienced the steepest decline (from 10.6 to -1.6) in March, followed by retail trade (from 1.3 to -6.1), while also manufacturing was strongly affected. At a more disaggregated level, travel agencies, tour operations, accommodation, publishing activities, and rental and leasing services experienced the sharpest drop (Figure 3). Turning to manufacturing (not shown in the chart), repair and installation of machinery and equipment, manufacture of leather and related products and production of motor vehicles, trailers and semi-trailers were the worst hit.

Table 1: Real GDP forecasts and post COVID-19 revisions (annual % change)

|

|

|

2020 |

2021 |

|||||

|

Region |

Source |

before COVID-19 |

post COVID-19 |

before COVID-19

|

post COVID-19 |

|||

|

World |

IMF |

3.3 |

|

|

|

|||

|

Goldman Sachs |

1.9 |

1.3 |

|

|

||||

|

Moody’s |

2.6 |

1.9 |

|

|

||||

|

his |

2.5 |

-2.8 |

|

3.3 |

||||

|

S&P |

- |

1 to 1.5 |

|

|

||||

|

Deutsche |

3.3 |

2.0 |

3.5 |

3.9 |

||||

|

IIF |

2.6 |

-4.1 |

|

|

||||

|

BNP |

2.8 |

0.5 |

3.2 |

4.4 |

||||

|

Natixis |

|

-2.9 |

|

2.8 |

||||

|

Euro Area1) |

IMF |

1.3 |

|

|

|

|||

|

Goldman Sachs |

1.0 |

-9.0 |

1.3 |

7.8 |

||||

|

ECB |

1.1 |

0.8 |

1.4 |

1.3 |

||||

|

Moody’s |

1.3 |

-2.2 |

|

2.0 |

||||

|

IHS |

0.0 |

-4.5 |

|

1.2 |

||||

|

S&P |

1.0 |

-0.5 to -1.0 |

1.2 |

1.5 |

||||

|

Deutsche |

1.0 |

-6.9 |

1.2 |

4.8 |

||||

|

IIF |

1.2 |

-5.9 |

|

|

||||

|

BNP |

0.8 |

-4.7 |

1.3 |

6.4 |

||||

|

Continuum Economics |

|

-0.3 |

|

1.1 |

||||

|

The Economist |

|

-5.0 to -10.0 |

|

|

||||

|

Natixis |

|

-5.9 |

|

4.4 |

||||

|

Memorandum items: real GDP growth |

||||||||

|

|

2009 |

|

||||||

|

EU |

-4.2 |

|

||||||

Notes: 1) From these institutions/banks/agencies, no forecasts are available for the EU yet.

Sources and dates of revised forecasts: IMF WEO (January), GS (March 17th (World) and 27th), ECB (March 12th), Moody’s (March 20th and March 26th), IHS (March 27th), S&P (March 3rd and March 17th), Deutsche Bank (March 18th (World), March 30th), IIF (March 23 and 25th), BNP (March 20th), Continuum Economics (March 21st) and Natixis (April 1st).

2. Policy response

EU member states have been actively intervening with economic measures to counter the crisis. New measures adopted by EU countries include:

- a voluntary postponement of the repayment of loans for six months, financial support for self-employed and temporary deferral of rents for companies in Czech Republic. In addition, the Czech Central Bank eased existing restrictions to conduct open market transactions.

- In Spain, the government announced to halt evictions, financial aid for temporary workers and interest-free micro-credit for tenants. The Spanish Central bank announced that the activation of counter-cyclical buffers for domestic lenders would not come into force for the next quarter.

- The Cypriot Central Bank communicated a series of measures to support those affected by the COVID-19 pandemic, including a pledge to provide liquidity and reductions in the costs of banking services.

- The German government said that it would provide a total of EUR 2bn in short-term financial assistance for startups struggling with the impact of COVID-19 but may not be eligible for other programs.

Beyond policy measures by individual member states, there is a strong need for a common, mutually reinforcing EU response to the crisis. European economies are strongly interconnected and a shock in any MS propagates to the rest of EU through labour movements, value chains, terms of trade and external demand. These spillovers can be quite large: besides the direct impact, a 1% decline in the GDP of Germany, France, Italy and Spain results in a further decline in the euro area’s GDP of 0.25%, 0.2%, 0.1% and 0.1 % respectively, merely on account of intra-euro area trade spillovers (European Central Bank (ECB), Monthly Bulletin 2013). Similarly, a positive shock in any EU country triggers positive impacts throughout the European Union. Macroeconomic modelling by the Economics Department of the EIB Group together with the Joint Research Centre of the European Commission shows that in the long run cross-country spillovers in the European Union explain, on average, 40% of the impact of the EIB investment on jobs and GDP inmember states. While smaller and more integrated countries gain relatively more, large EU countries also greatly benefit from positive spillovers (in Germany, for instance, they account for more than 30% of the total impact of EIB investment on jobs). On top of trade links, EU countries are also deeply interconnected via financial markets and confidence feedback loops. Taking these spillovers into account when designing the EU response to the unprecedented crisis we are facing is crucial: leveraging on additional and mutually reinforcing effects, a joint EU response can reach far and above what any individual MS can achieve alone.

Steps to strengthen the joint European response to COVID-19 have intensified this week. Following the invitation by the European Council, the Eurogroup has continued preparatory work on proposals to develop pan-European financial responses, to be discussed on April 7. In the public discussion, several ideas continue to be debated, including the enhanced use of the ESM credit lines, common bond issuance, an enhanced role of the EIB via a guarantee fund to support corporates, as well as possible avenues to deploy the next MFF in support of recovery. Given that different measures also address different problems stemming from the crisis, including short-term liquidity constraints and mid-term needs to finance the recovery, combinations of instruments could provide for a forceful response to increase the block’s economic resilience and prospects for recovery.

The EC approved several national schemes to support firms and mitigate the economic impact of the pandemic, proposed additional support to the healthcare systems mobilising EUR 3bn from the EU budget for emergency support and medical equipment, and presented a proposal for temporary support to mitigate unemployment risk in an emergency (SURE). SURE will assist with loans of up to EUR 100 bn, supporting member states in addressing higher public expenditure to preserve employment. The scheme aims to help cover the costs of setting up or extending short-term work schemes and similar measures. Supported by a system of voluntary guarantees, the Commission will on-lend to member states requesting support on favourable conditions. While still pending approval and envisaged as a temporary measure, SURE can help to mitigate protracted divergences across European labour markets as experienced in the years following the financial crisis providing support for employment across the European Union.

In the United States, the Fed eased a capital rule for large banks, intending to stimulate banks to lending more and play a more prominent role in the US Treasury market. The “supplementary leverage ratio” was a rule adopted in 2013 and required large banks with international portfolios to hold capital (equal to 3% of total assets) to absorb losses. The Fed stated that now banks can exclude Treasuries and cash reserves held at the Fed from these calculations for a year. This way, the Fed pushes more cash reserves into the banking system: the banks will be able to take those reserves on to their balance sheets without having to increase capital at the same time.

The IMF has received requests for aid to deal with the coronavirus from more than 80 countries (50 emerging countries and 31 middle-income countries), totalling more than USD 20bn. This is less than half of the USD 50 billion in support that the fund made available in rapid emergency financing for low-income and emerging markets. However, the Fund sees developing nations needing USD 2.5tr in financial support to fight the coronavirus. Among the countries, Argentina is pursuing a restructuring, Ecuador is discussing a re-profiling, and Zambia is seeking to restructure its foreign bonds. Pressure on developing economies’ financial assets is expected to continue as several economies need to repay dollar-denominated government debt coming due in the second quarter of 2020.

The first World Bank emergency funds have been approved to help developing countries fight the pandemic. The envelope with USD 1.9bn lending capacity to support projects in 25 countries and project in another 40 countries is close to approval. Of the 76 low-income countries qualifying for assistance under IBA, 40 had also applied for assistance.

3. Financial markets

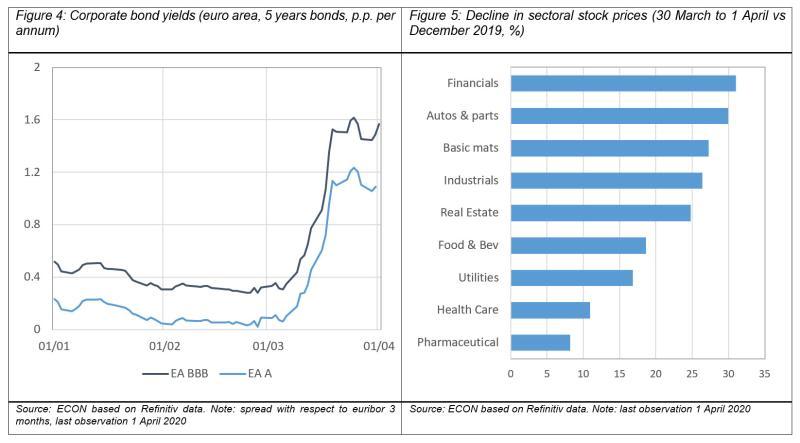

The corporate sector showed some signs of (temporary) sstabilisation this week, though at high levels, while sectoral differences remain visible. Non-financial corporate stock prices have hovered around the level reached last week, 25% below December 2019, but 10% above the trough of two weeks ago according to the data until April 1. Between-day volatility, though, persisted. Importantly, corporate stock prices have decoupled from banks’ stock prices as of last week. After resuming their decline, banks´ stock prices have been hovering around a level similar to their previous low reached around the 20th March. The overall decline in corporate stock prices is uneven across sectors. Passenger airlines, tourism, automobile, hotels and restaurants and non-food retail sector are the most exposed sectors, while pharmaceuticals, health care, utilities, energy and digital are more cushioned (Figure 5).

Credit risk spreads have also stabilised over the last two weeks, after having gone substantially up during the first half of March – from 0-40 to 120-160 bps for corporates rated A to BB, and bonds of 5-years maturity (Figure 4). Currently, corporate bonds spreads – vis-à-vis monetary policy rate – stand less than half-way from their peak reached during the Lehman crisis, in the beginning of 2009.

Corporates have actively tapped the bond market not only in the United States but also in Europe. Issuance by investment-grade companies reached USD 259bn in the US (a new monthly record) and EUR 135bn in Europe (the most since 2016). Moreover, this trend in Europe intensified last week with 17 deals issuances last Wednesday, totalling EUR 26.8bn.

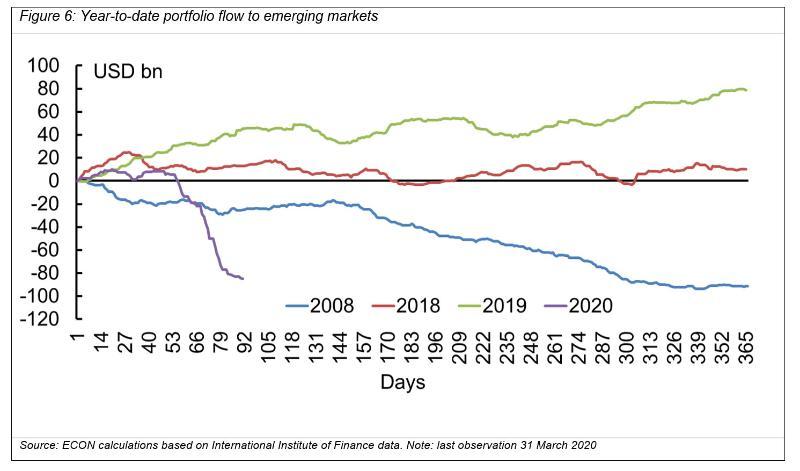

The performance of emerging markets has remained weak and capital outflows are reaching record levels. Emerging market stocks and currencies continued their slide during the week. The stimulus packages put forward by central banks and governments across the globe did not deter international investors from fleeing emerging market assets. Since the beginning of the year, a record USD 83.3bn have flown out emerging market equity and debt markets, according to the Institute of International Finance (IIF). This is a considerably sharper outflow than those seen during the 2008 financial crisis, the “taper tantrum” in 2013 and the 2015 Chinese yuan devaluation scare (chart below), implying a sudden stop in emerging markets due to the combination of uncertainty around the spread of coronavirus and large oil price and financial shocks (Figure 6).

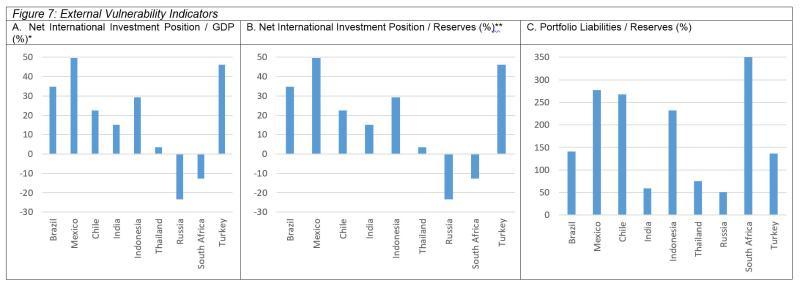

To gauge the resilience of emerging markets’ external balances, some indicators of external liabilities and reserves for nine systemically important emerging markets are presented below. According to the data, among the selected countries, Turkey, Brazil and Mexico have the highest external indebtedness relative to their national income (Figure 7, A). Excluding FDI stocks, reserve assets of all selected countries are high enough to cover net liabilities (Figure 7, B). . However, no countries except for Russia and Thailand would be able to cover a sudden reversal in portfolio flows with its own reserves (Figure 7, C). That said, Thailand’s economy has proved to be quite resilient so far, but it will likely suffer from the COVID-19 crisis on the back of shrinking tourism revenues. As for Russia, the extreme volatility in its financial indicators is related to the heavy dependence of the country on oil revenues for both fiscal revenues and external accounts.

4. European Banks in focus: are they resilient to the COVID-19 crisis?

This section zooms in on the European banking sector, trying to understand how well-placed banks are to cope with the ongoing crisis. We do so by comparing the current situation with past crisis episode.

(1) Banks are better placed to withstand the shock than in 2008.

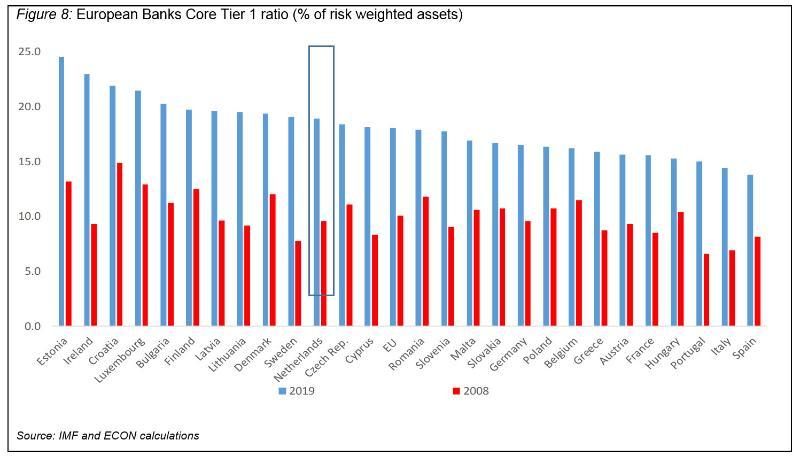

European banks’ capital position is now substantially more robust than in the previous crisis. Core tier 1 capital stands now at 18% of risk weighted assets for the EU average, 8 p.p. higher than in 2008 (Figure 8). Moreover, while this aggregate figure masks some notable differences across countries, the countries that currently have a weaker capital position are still in a much stronger position than before the onset of the global financial crisis. The Single Supervisory Mechanism makes explicit reference to the fact that banks have enough buffers (for capital and liquidity) and therefore should use them (more details on point (3) below).

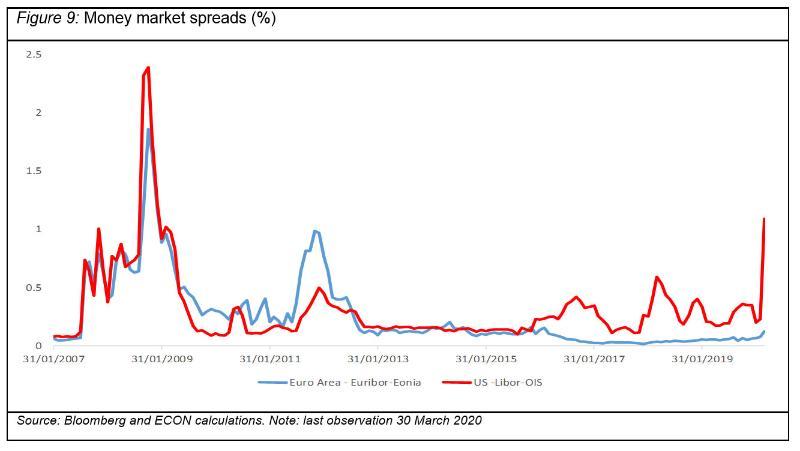

Funding markets for banks are showing some signs of distress, but the current situation is different from what was experienced in the global financial crisis. In 2008/2009, banks faced real liquidity constraints that are now almost residual: central banks have been more proactive in providing liquidity than in 2008/09. The ECB is now offering long term unlimited funding through different instruments. Money market spreads, usually a measure of liquidity risks, show no signs of stress in the euro area (Figure 9). Further, while there are still some signs of stress in the United States, with the biggest increase in spreads since the 2008-2009 financial crisis, current spread levels are still far from the levels registered back then. Moreover, these spikes can largely be attributed to the increasing demand for US dollars, the global funding currency.

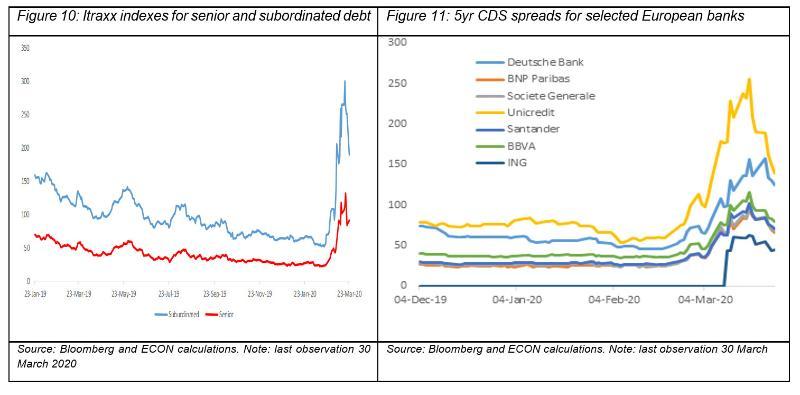

European financial institutions’ credit risk increased somewhat as measured by financial market indicators such as the Itraxx indexes (which are a measure of credit risk represented by an average of CDS spreads of the main European banks for senior and subordinated debt). These indexes have been increasing substantially since late February but registered a relative decline in the past week (Figure 10). The picture is relatively common across some of the main European banks. Still, banks show a different credit risk depending on the country where they concentrate their operations and on their or idiosyncratic issues (Figure 11).

2) This time is different: the crisis is a global health crisis hitting the real economy hard, but it did not originate in the banking sector. Yet, spillovers could be severe.

The current crisis had its origin in the real side of the economy. In contrast, the 2008 global financial crisis started in the financial sector and therefore led to significant losses through exposure to financial markets. Hence, it is plausible to assume that losses could be more contained. Yet, given the potential severity of the recession, banks may still face significant strains, both through a deterioration in financial markets and credit asset quality (NPLs).

Following the 2008 crisis, European banks experienced further losses through their exposure to sovereigns. A repetition of this “doom loop” cannot be entirely excluded at this stage, as shown by the increase in sovereign bond yields in the first weeks of March. Nevertheless, the prompt policy intervention of the ECB and the policy packages put in place by national authorities have so far provided much-needed support to both banks and sovereigns (See Section 2 of weekly briefings).

Non-performing loans are expected to increase at a faster pace than in past crisis episodes given that the expected fall in GDP could be much bigger, concentrated in time and broad based (households, micro, small and medium enterprises and corporates are all taking a hit and many economic sectors are going to be affected simultaneously). Non-performing loans tends to lag GDP growth by 12-18 months, but this time the reaction function could be steeper as entire economies across Europe (and the world) come to a (almost) sudden stop. Still, this increase is likely to be more concentrated in some sectors and could potentially be reversed, if GDP growth recovers in 2021. This seems the most likely scenario if containment measures are effective at eventually halting the virus spread and policy support measures are swiftly implemented to mitigate the economic fallout.

3) Policy matters: measures proactively implemented by central banks and financial regulators can go a long way in strengthening banks’ resilience to the crisis. But more is needed to support the real economy.

Several policy measures have been implemented already at EU level and by MS to help mitigate the impact of the crisis on the capital position of European banks (See also Section 2):

Dividend freezes - The ECB updated its recommendation to banks on dividend distributions. To boost banks’ capacity to absorb losses and preserve their capita position, they should not pay dividends for the financial years 2019 and 2020 until at least 1 October 2020. Banks should also refrain from share buy-backs aimed at remunerating shareholders. Some national regulators also introduced similar measures.

Credit guarantees - An unprecedented broadening of credit guarantee instruments have been announced by various MS, as well as by EU institutions, including the ECB. Such guarantees can help to take some of the increased credit risk off the balance sheet of the banking system and provide capital relief at the same time. The ECB announced that loans that become non-performing and are under public guarantees would benefit from preferential prudential treatment in terms of supervisory expectations about loss provisioning.

Treatment of compulsory loan repayment moratoria - The European Banking Authority stated that generalised payment delays due to legislative initiatives and addressed to all borrowers should not lead to any automatic classification as default, forborne or unlikeness to pay. Individual assessments of the likelihood to pay should be prioritised.

Flexible use of existing capital buffers - Capital and liquidity buffers have been designed to allow banks to withstand stressed situations like the current one. The European banking sector has built up a significant amount of buffers since the last crisis, but various measures were now allowed1. Relaxation of the capital buffers does not improve the capital position of the banks per se. However, flexibility by the regulators limits the potential stigma associated with using these buffers, and the possible negative market reactions.

Limiting pro-cyclical assumptions in loan loss provisioning - To avoid excessive pro-cyclicality in the regulatory capital and published financial statements, the ECB recommends that all banks avoid pro-cyclical assumptions in their models to determine provisions.

To summarise, we argue that while the current economic shock poses significant risks for banks, a number of factors could mitigate the negative impact. In comparison to the 2008-2009 financial crisis, we note that: (a) the initial shock will most likely be shorter if the policy response remains strong, timely and well-targeted, (b) the crisis is not originating in the banking sector, (c) banks have sounder capital and liquidity positions than in 2008 on the back of the policy and regulatory measures undertaken following the financial crisis. On the other hand, the contraction in GDP may be more significant than during the global financial crisis and could trigger a more immediate impact on non-performing loans, as entire economies are being shut down. All in all, we expect European banks to remain resilient. Yet, uncertainty remains huge, and a prolonged or sharper recession would not leave banks unscathed.

1) For example, it allows them to operate temporarily below the level of capital defined by the Pillar 2 Guidance (P2G), the capital conservation buffer (CCB) and the liquidity coverage ratio (LCR). These measures are enhanced by the relaxation of the countercyclical capital buffer (CCyB) by the various national macro-prudential authorities. In addition, banks will also be allowed to partially use capital instruments that do not qualify as Common Equity Tier 1 (CET1) capital, such as additional Tier 1 or Tier 2 instruments, to meet the Pillar 2 Requirements (P2R).

5. Conclusions

Economic data continues to be bleak. Therefore, a targeted, credible, coordinated and fast policy action is required at the EU and the country level. Second, policy response as pivotal as it is also helping to calm financial markets. This is important as EM have in principle less firepower to safeguard their economies as they are also experiencing substantial portfolio outlaws. That said, volatility is likely to remain elevated in coming weeks, while the unemployment is expected to soar further.

The immediate effects of the crisis may appear local, but in a highly interconnected European economy their ripple effects will be felt throughout Europe. This was revealed clearly during the global financial crisis. Today, banks entered into the storm with a strong fleet and already received substantial support from policymakers. That said, waters could become even choppier than currently expected.

Table 2: GDP forecasts and post COVID-19 revisions – selected countries

|

|

2020 |

2021 |

|||

|

Country |

Source |

Before COVID-19 |

Post COVID-19 |

Before COVID-19 |

Post COVID-19 |

|

Italy

|

IMF |

0.5 |

|

|

|

|

Goldman Sachs |

0.2 |

-3.4 |

|

|

|

|

IHS |

-0.1 |

-3.5 |

|

|

|

|

S&P |

0.2 |

-11.6 |

0.6 |

1.0 |

|

|

Deutsche |

0.5 |

-8.7 |

0.6 |

4.1 |

|

|

Continuum Economics |

- |

-1.7 |

|

0.8 |

|

|

Moody’s |

|

-2.7 |

|

2.1 |

|

|

Prometeia |

0.1 |

-6.5 |

|

|

|

|

Natixis |

|

-7.3 |

|

2.5 |

|

|

Germany |

IMF |

1.1 |

- |

|

|

|

Goldman Sachs |

0.9 |

-8.9 |

1.4 |

8.5 |

|

|

IHS |

0.4 |

-1.2 |

|

|

|

|

S&P |

0.5 |

0.0 |

1.0 |

1.5 |

|

|

Deutsche |

1.0 |

-5.3 |

1.1 |

5.4 |

|

|

Continuum Economics |

- |

-0.3 |

|

1.1 |

|

|

Moody’s |

|

-3.0 |

|

2.5 |

|

|

Natixis |

|

-6.7 |

|

6.3 |

|

|

France |

IMF |

1.3 |

- |

|

|

|

Goldman Sachs |

1.1 |

-7.4 |

1.4 |

6.4 |

|

|

IHS |

0.8 |

-0.6 |

|

|

|

|

S&P |

1.3 |

0.7 |

1.3 |

1.7 |

|

|

Continuum Economics |

- |

0.0 |

- |

0.9 |

|

|

Moody’s |

|

-1.4 |

|

1.8 |

|

|

Deutsche |

|

-6.8 |

|

4.2 |

|

|

Natixis |

|

-4.5 |

|

4.0 |

|

|

Spain |

IMF |

1.6 |

- |

|

|

|

Goldman Sachs |

1.8 |

-9.7 |

1.7 |

8.5 |

|

|

IHS |

1.7 |

-1.8 |

|

|

|

|

S&P |

1.7 |

1.3 |

1.6 |

1.9 |

|

|

Continuum Economics |

- |

-0.2 |

|

0.8 |

|

|

Deutsche |

|

-8.7 |

|

5 |

|

|

Natixis |

|

-4.2 |

|

2.7 |

|

|

Portugal |

BdP |

1.7 |

-3.7 |

1.6 |

0.7 |

|

Czeck Republic |

IIF |

2.6 |

-5.4 |

|

|

|

BNP |

2.7 |

-1.0 |

3.0 |

7.0 |

|

|

Hungary |

IIF |

3.0 |

-6.0 |

|

|

|

BNP |

3.1 |

-1.5 |

3.6 |

6.0 |

|

|

Poland |

IIF |

3.9 |

-6.4 |

|

|

|

BNP |

3.3 |

0.5 |

3.4 |

6.0 |

|

|

Romania |

IIF |

3.4 |

-6.1 |

|

|

|

BNP |

3.0 |

-2.0 |

3.5 |

7.0 |

|

|

Slovenia |

MIoS |

1.5 |

-6.0 |

2.2 |

|

|

UK |

Moody’s |

|

-2.6 |

|

2.4 |

|

Goldman Sachs |

1.0 |

-7.5 |

2.1 |

7.3 |

|

|

IHS |

|

-4.3 |

|

0.8 |

|

|

Deutsche |

|

-6.5 |

|

5.2 |

|

|

Natixis |

|

-5.0 |

|

3.7 |

|

|

China |

IMF |

6 |

- |

|

|

|

Goldman Sachs |

5.5 |

3.0 |

|

|

|

|

Moody’s |

6.2 |

3.3 |

|

6.0 |

|

|

IHS |

5.8 |

2.0 |

|

6.4 |

|

|

S&P |

- |

2.7-3.2 |

|

|

|

|

Deutsche |

6.1 |

1.0 |

6.0 |

10.0 |

|

|

IIF |

5.8 |

2.8 |

|

|

|

|

BNP |

5.7 |

2.6 |

5.8 |

7.6 |

|

|

Continuum Economics |

- |

5.3 |

|

6.0 |

|

|

Natixis |

|

3.0 |

|

5.5 |

|

|

US |

IIF |

1.5 |

-4.9 |

|

|

|

Goldman Sachs |

2.3 |

-3.8 |

2.4 |

5.3 |

|

|

Continuum Economics |

|

-0.7 |

|

2.9 |

|

|

BNP |

1.5 |

-0.7 |

2 |

2.4 |

|

|

Moody’s |

1.8 |

-2.0 |

|

2.3 |

|

|

Deutsche |

1.9 |

-0.8 |

2.1 |

2.4 |

|

|

S&P |

1.9 |

1.6 |

|

|

|

|

The Economist |

|

-5.0—10.0 |

|

|

|

|

Natixis |

|

-5.1 |

|

0.7 |

|

Sources and dates of revised forecasts: IMF WEO (January), GS (March 17th (World) and 27th), ECB (March 12th), Moody’s (March 20th and March 26th), IHS (March 19th), S&P (March 3rd and March 17th), Deutsche Bank (March 18th (China and US), March 30th), IIF (March 23 and 25th), BNP (March 20th), Continuum Economics (March 21st), Banco de Portugal (March 26th), Macroeconomic Institute of Slovenia (March 23rd), Prometeia (March 28th) and Natixis (April 1st).